Motorola Solutions, Inc. (MSI)

")

Company Description

Motorola Solutions MSI 0.00%↑ is a global leader in public safety and enterprise security technology. Originally founded in 1928 as Galvin Manufacturing Corporation, by two brothers, Paul and Joseph Galvin, the company made its mark by creating the first car radio, but was rebranded in 1947 to Motorola. After years of evolving the company was eventually split into two entities in 2011; Motorola Mobility, which focused on mobile phones and was later sold to Google, and Motorola Solutions, which kept the ticker MSI and ultimately became the legal successor to the original Motorola. Currently, MSI 0.00%↑ specializes in critical communication equipment, video security, and software solutions. Motorola Solutions has a current market cap of just over $70B, and employs approximately 21,000 people. The stock has performed exceptionally well over the past decade, with a total return of more than 660%, equating to a remarkable CAGR of 22.6%.

Additionally, here are some of Motorola Solutions financial metrics.

Quality Financial Metrics

As always, this section is where I discuss some financial metrics I deem to be important in deciding if the company is a high-quality business.

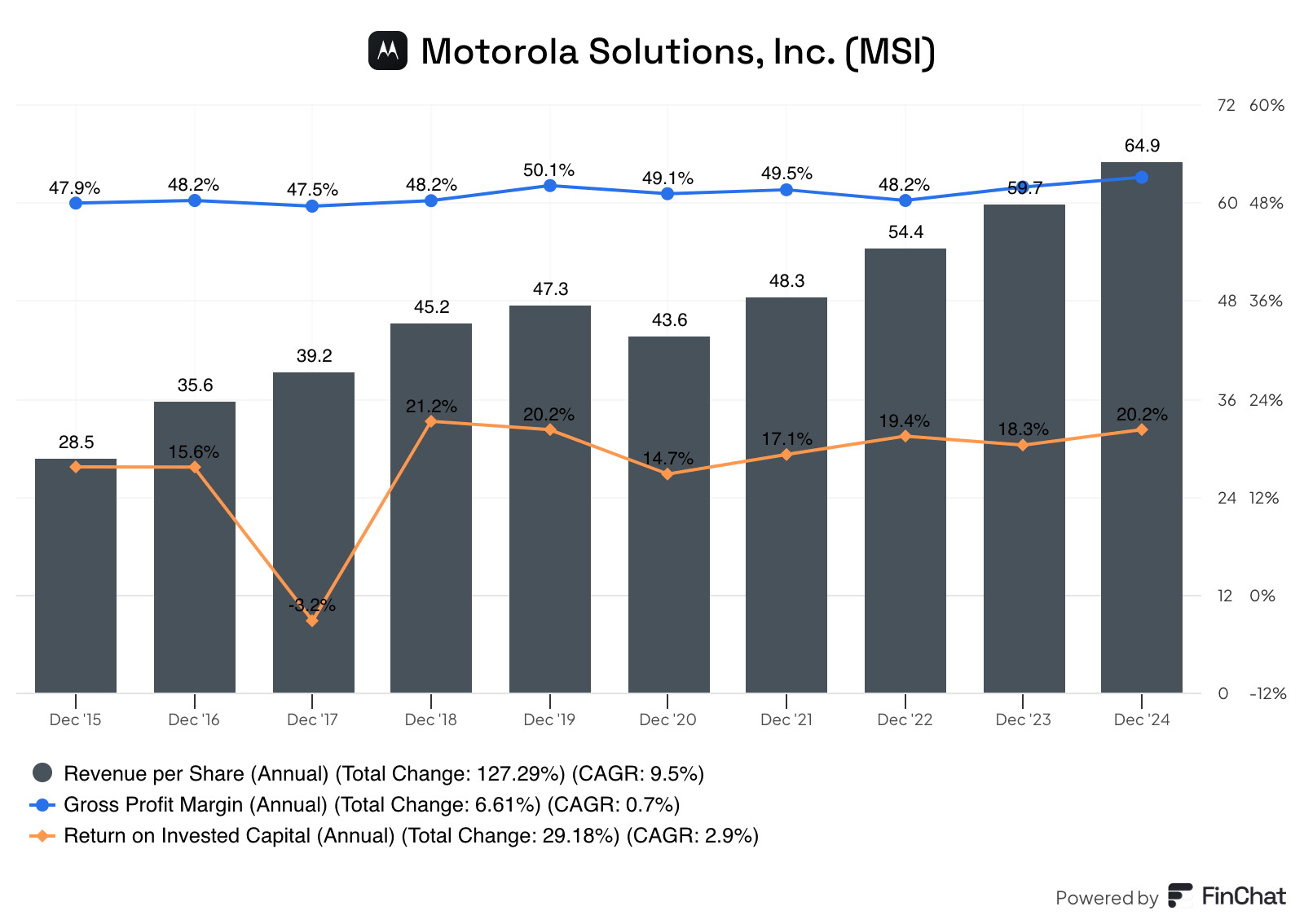

The revenue per share for MSI 0.00%↑ looks like two sets of stairs. From 2015 through 2019, the company was on a solid upward trend growing at about 13.5% annually during that timeframe. The pandemic caused a minor setback in 2020 with the RPS metric dropping about 8%. However, the following year the company picked up where it left off, and has grown its revenue per share by more than 10% annually, post pandemic.

The blue line below represents the gross profit margin, which has remained remarkably steady. It fluctuates slightly from year to year but has generally hovered around 50%; even eclipsing 51% in the most recent fiscal year. There isn’t much to analyze about this metric, given its consistent stability.

The return on invested capital metric for MSI 0.00%↑ is one of the better ones I’ve seen since I started doing these company reviews, with 2017 being a clear outlier. Aside from that year, MSI 0.00%↑ has done an outstanding job creating value for its shareholders, with its ROIC well-above its cost of capital. I usually aim for companies with a ROIC close to 20%, and Motorola Solutions doesn’t disappoint.

There isn’t a lot to harp on with these financials, the revenue is growing, the gross profit margin is ever-improving, and the return on invested capital is routinely at a healthy level. MSI 0.00%↑ has some phenomenal financials, and investors should definitely monitor this dividend-grower.

Dividend Data

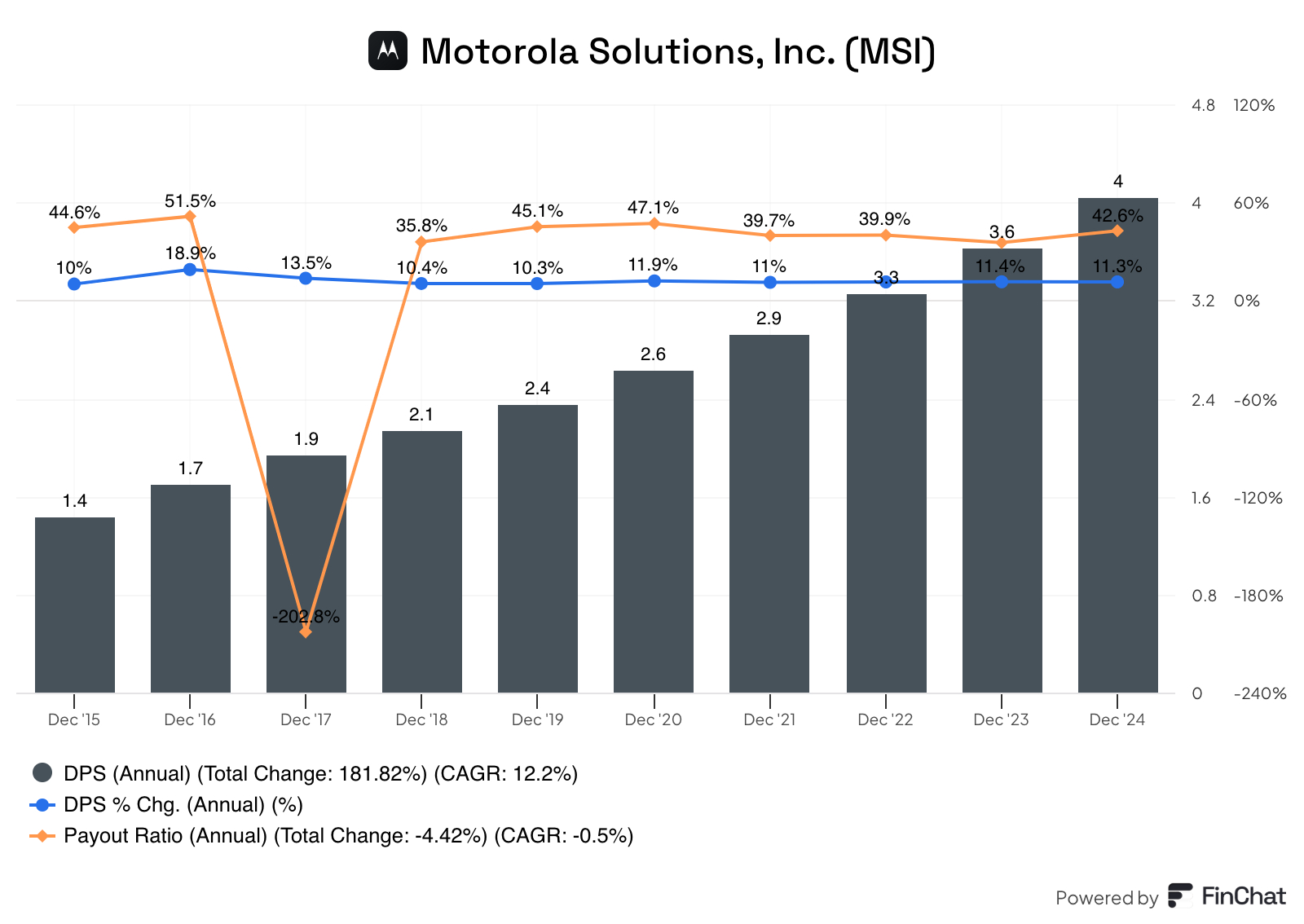

Speaking of dividends, MSI 0.00%↑ currently pays a quarterly dividend of $1.09 per share, resulting in an annual payout of $4.36, and a yield of about 1%. Over the past decade, the dividend growth has been solid and consistent, coming in at about 12% per year. Lastly, the payout ratio, has trended lower over the years, going from a chart high of 51.5% in FY2016 to 42.6% just last year. The company has plenty of room to continue growing its dividend, and there’s no reason they shouldn’t continue to do so for the foreseeable future.

Risks

Being in the technology space on a worldwide level, Motorola has some unique challenges they could face. Let’s take a look at what I think are some of their potential headwinds.

Technology is advancing at an unprecedented pace, and the field MSI 0.00%↑ operates in is no exception. The mission-critical communications and security space is getting crowded, with rivals like Axon Enterprise AXON 0.00%↑ (body cameras, software) and Nokia NOK 0.00%↑ (private networks) vying for their share of the market. Motorola must continually innovate new and differentiated products to keep up with ever-changing technologies.

Another potential problem MSI 0.00%↑ could face is their high customer concentration. The company relies heavily on a few major clients, most notably the U.S. government as well as the U.K. Home Office, which together account for a significant portion of their revenue. This concentration heightens their vulnerability, should either client reduce spending, delay payments, or shift priorities, it could be disastrous for Motorola.

The final headwind I’d like to discuss is specific to companies that operate on a worldwide basis. In the company’s most recent earnings report, management cited currency fluctuations as a persistent problem, with an anticipated $120 million in unfavorable foreign exchange impacts for 2025. Obviously, this is something a lot of companies have to manage but a $120M impact from unfavorable foreign exchange seems awfully high.

These are just a few of the potential risks related to a position in MSI 0.00%↑. However, with constant changes in the landscape, it’s essential to stay updated on news and M&A transactions related to the company to fully understand its business and make an informed decision regarding a potential investment.

Recent Earnings

In mid-February, MSI 0.00%↑ announced 4Q24 earnings, as well as full year results, we’ll start with the quarter earnings report.

Motorola had Non-GAAP earnings per share of $4.04 which beat the consensus estimate by $0.15, on revenue of $3B, which was in-line with expectations, and a 5.6% increase compared to the prior year. GAAP EPS came in at $3.56, a 3% increase from Q4 2023, with operating earnings rising 10%, to $814M for the quarter.

Looking at the segments, the Products and Systems Integration Segment saw sales climb 3% to $1.95B, with GAAP operating earnings of $541M and Non-GAAP operating earnings of $594M. The Software and Services Segment had revenue surge 11% to $1.06B from $958M for the prior year. GAAP operating earnings also rose by 11% percent, with Non-GAAP operating earnings increasing 6%.

For the year, sales were $10.8B, an 8% increase YoY, resulting in GAAP EPS of $9.23, a 7% decline from the prior year, while Non-GAAP EPS grew by 16% to $13.84 per share, from $11.95 in 2023.

Again, looking at the segments, the Products and Systems Integration segment saw sales rise 10% for the year to $6.88B, with its counterpart, the Software and Services segment growing by 5% to $3.9B.

Some other notable news from the press release was the company backlog rising to a record $14.7B, up 3% from the end of 2023. Operating cash flow for the fiscal year surged 17% to $2.4B, and free cash flow for the year was a record $2.1B.

Finally, MSI 0.00%↑ paid $654 million in dividends for the year and repurchased $244M worth of its common stock at an average cost of $396.69 per share (as a reference the current price is approximately $436/share).

Overall, the earnings report was not well-received by the market with the stock dropping about 6%. The full earnings call can be read/listened to here.

Valuation

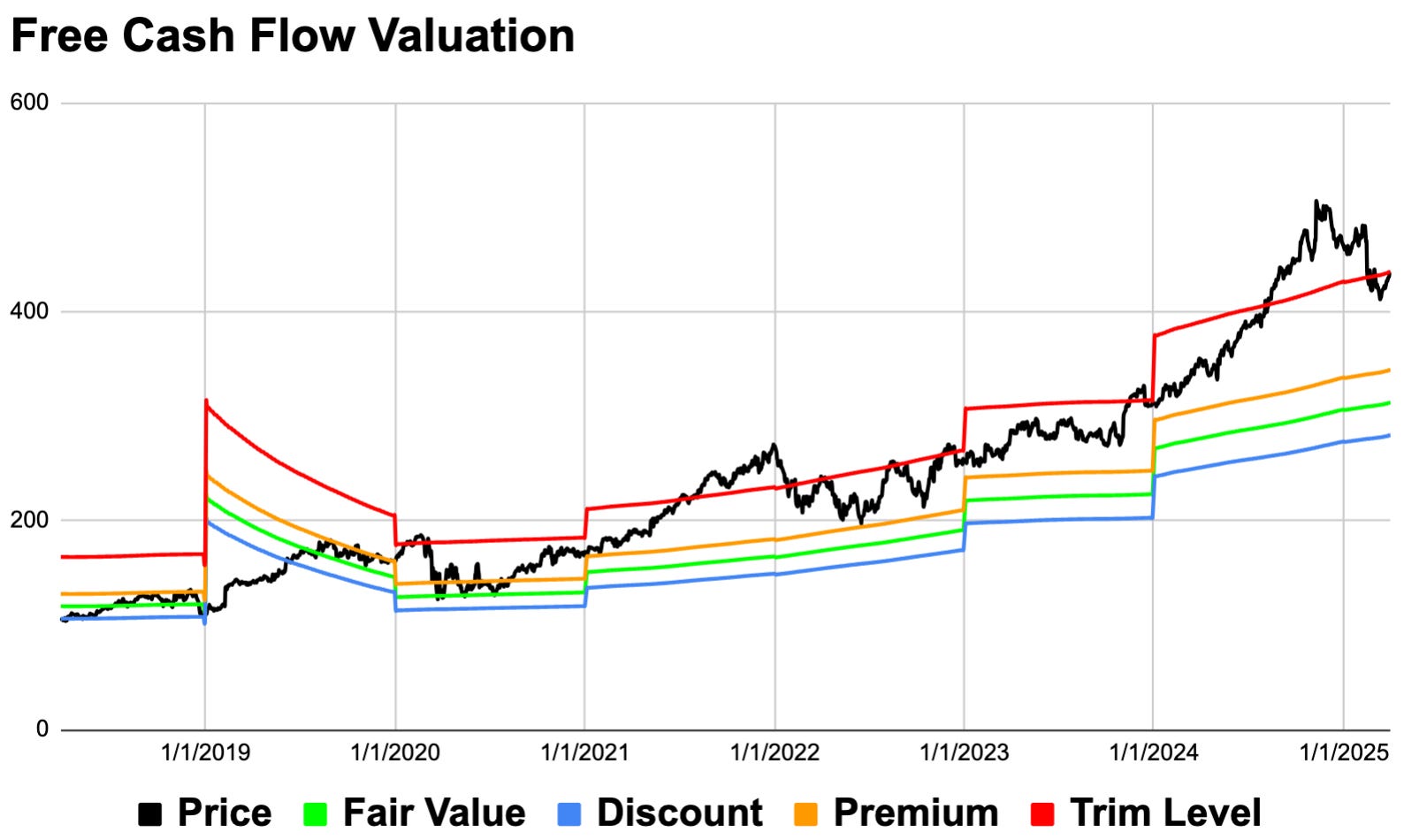

As you know by now, the last piece of a deep dive is to determine if the company is potentially overvalued or undervalued. To do so, let’s examine it from a free cash flow perspective.

As you can see, MSI 0.00%↑ rarely trades for a discount, and unfortunately, now is no different. Looking back, the stock traded for a slight discount during the first half of 2019, but by the end of the year was trading for a premium. Covid caused a quick drop in 2020, but even then the stock didn’t trade for a discount. In 2021, the stock surged more than 60% and was grossly overvalued by year-end. The FCF was basically flat in 2022, as was the stock price, dipping only 4%. Over the next two years Motorola had free cash flow growth of 14.64% and 19.29%, respectively, and the stock responded by climbing 23% and nearly 50%, respectively. This leads us to where the stock is now trading, for a massive overvaluation relative to its FCF, even after the stock losing about 5% year-to-date.

The company has a rough long-term expected rate of return of just 1.86% with the components of that estimate being at 1% dividend yield, a -6.81% return to fair value factor (thanks to the drastic overvaluation), and a 7.67% expected earnings growth rate.

In summary, the stock has performed very well since its spin-off, topping the broad market by a good margin. The financials are some of the best I’ve seen and the dividend growth is consistently above double-digits. The risks are hard to ignore, but the company has done well to weather them so far during its existence, so I have faith they’ll continue to do so. For me, it really comes down to the valuation, according to my chart above the stock is trading for nearly 40% above its fair value, and thus, investors should wait for a significant pullback before initiating or expanding a position. However, with all that being said, this is definitely a company worth keeping an eye on, as aside from the valuation, everything else checks out.

If you found this content insightful consider upgrading to a paid subscription, you can see live valuation ratings here, at any time. Additionally, you’ll gain access to a live complimentary Free Cash Flow Valuation Tool for over 200 stocks, as well as access to our 3 model portfolios. The paid subscription is only $5 per month and you can cancel any time.

In case you miss them, here are some recently covered stocks:

Old Dominion Fright Line ODFL 0.00%↑

Moody’s Corporation MCO 0.00%↑

Check out some tools to help with your investing journey

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin