Old Dominion Freight Line, Inc. (ODFL)

")

Company Description

Old Dominion Freight Line, ODFL 0.00%↑, is a leading shipping company that specializes in transporting smaller freight shipments that don’t require a full truckload, offering regional, inter-regional, and national services across the United States, Mexico, and Canada through partnerships. ODFL 0.00%↑ has a market cap of more than $35 billion and currently employs slightly more than 20,000 people. Over the past decade, the stock has delivered a total return of more than 550%, resulting in a market-beating CAGR of 20.5%.

Additionally, here are some of Old Dominion’s current financial metrics.

Quality Financial Metrics

As you know, I review three financial metrics to determine if a company is of high-quality. I want to see the company’s revenue growing, a reliable gross profit margin, and a healthy return on invested capital. Let’s examine ODFL 0.00%↑ and see how their financial metrics measure up.

The revenue per share for ODFL has has some good years and some mediocre ones. There was minimal change between 2015 and 2016, followed up by impressive increases of 13.4% and 21% in 2017 and 2018, respectively. ODFL didn’t see another substantial increase until 2021, when its RPS surged 33.3%, and again in 2022, when it climbed 22.6%. However, in 2023, it dipped slightly, and it rose only minimally last year. This could be somewhat worrisome if this metric doesn’t rebound, as the company typically reduces its share count by at least 1% per year—sometimes more, including in 2022, where it shrank by more than 4%.

The gross profit margin for ODFL 0.00%↑ has been increasing ever year for the past decade, with 2024 being a minor exception. The company has clearly done a tremendous job at creating operational efficiencies and implementing effective cost management through various initiatives. ODFL 0.00%↑ should continue to remain lean in its operations and work to further expand its GPM.

Similar to the gross profit margin, the return on invested capital has also improved over the years, though with a bit more volatility. From 2015 through 2017, the ROIC was a respectable 13% to 18.4%, before exceeding 20% in FY 2018 and 2020 (and coming close in 2019). Following the pandemic, the ROIC climbed even higher, surpassing 35% in FY22. Since then, it has settled at still very healthy levels, including 28.4% in 2023 and 24.9% just last year.

The main concern with ODFL 0.00%↑ is its revenue per share. While it’s been on an upward trend overall, it has slipped the past couple of years and isn’t rising at a consistent rate. This is likely not a major issue, but it’s something investors should be aware of moving forward. Regarding the GPM and ROIC, ODFL 0.00%↑ should continue its successful strategies, which have worked well over the years. Old Dominion is definitely a high-quality business that investors should keep an eye on.

Dividend Data

As you can see from the chart below, Old Dominion has not paid a dividend for very long. However, it has grown substantially, from 2017 when the company paid about $0.13 per share, to last year, when it pad $1.02 per share for the year. The increases have been very impressive, although, to be fair, it’s easier to achieve eye-catching growth rates when the company starts with a low dividend. In fact, the chart below indicates a dividend growth CAGR (since inception) of 34.1%. However, I did a little more research and found the company has already announced their dividend increase in 2025, which is 7.7%— still very good, but nothing compared to its historical growth. Don’t get me wrong; I’m not knocking their dividend growth thus far—far from it. It’s just important to see the whole picture and recognize that growing their dividend at a rate of 30% or more annually isn’t realistic long-term. Lastly, the payout ratio is very low, which makes sense given their short history, this should allow for solid dividend increases moving forward.

Potential Headwinds

Old Dominion operates a vast fleet of trucks across the nation and has done well since its humble beginnings. Let’s take a look at some of potential problems the company could face if they don’t remain competitive.

Rising operating costs is a major one since fuel, labor, and equipment aren’t cheap, and costs can spike quickly. The main driver in this arena, is the cost of fuel, which ODFL 0.00%↑ uses surcharges to offset them, but dramatic increases could take a toll on their margins, especially if customers push back. Along those same lines, are labor costs, and specifically the costs to acquire and keep their workforce. For a while now, the trucking industry has faced a persistent driver shortage, due to an aging workforce, tough working conditions, and competition from other sectors. ODFL 0.00%↑ will have to remain agile to the ever-changing conditions in their industry to stay competitive to their customers and their employees.

Another clear headwind for ODFL 0.00%↑ is relying on the global supply chain and dealing with disruptions, either short term or long. Global events such as a pandemic or trade wars which distract supply chains, hurting freight volumes and creating unpredictable demand swings. Although Old Dominion has an extensive network, which helps, it’s not immune to bottlenecks or delays outside of its control.

These potential headwinds are just a few that I dove into, some other notable problems they could face are innovation risks such as keeping up with technology and utilizing route optimization. Furthermore, AI is becoming evermore prevalent in our world, and I don’t think it’s unrealistic for ODFL 0.00%↑, or the trucking industry as whole, to be disrupted in the near future with AI driven logistics.

Recent Earnings

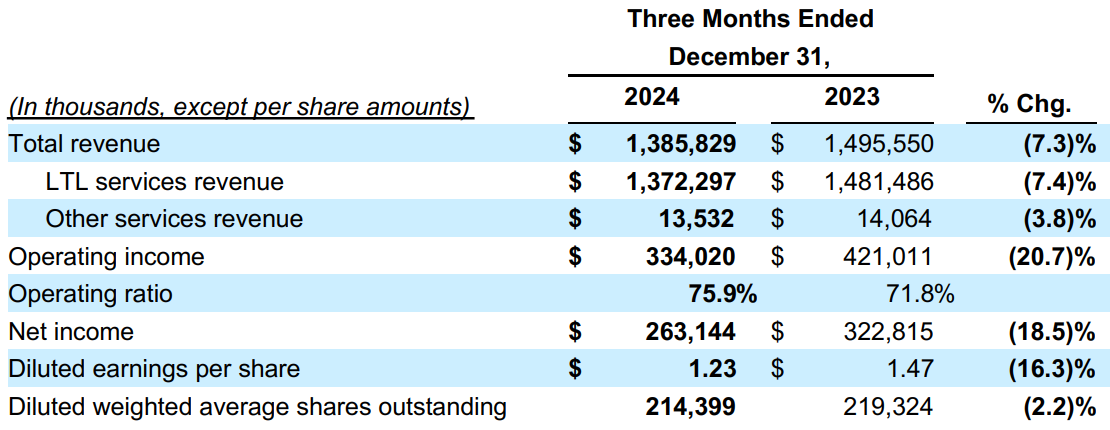

A few weeks ago ODFL 0.00%↑ announced their 2024 Q4 earnings with a double beat. GAAP EPS beat estimates by $0.07, coming in at $1.23 per share on revenue of $1.39B which also exceeded expectations by $10M, but was a YoY decrease of 7.3%.

As indicated on the chart below, LTL revenue declined 7.4%, while other revenue dipped 3.8% year-over-year. Additionally, their operating income dropped more than 20% to $334M for the quarter but their operating ratio expanded by more than 400 bps.

As previously mentioned, the company raised its dividend during this earnings call as well by 7.7%. Finally, ODFL 0.00%↑ announced they spent nearly $970M on share repurchases for the year, while also distributing almost $225M in dividends.

The full earnings call can be listened to here.

Valuation

As you know, the last piece of this puzzle is diving into whether or not the company is trading for a fair valuation.

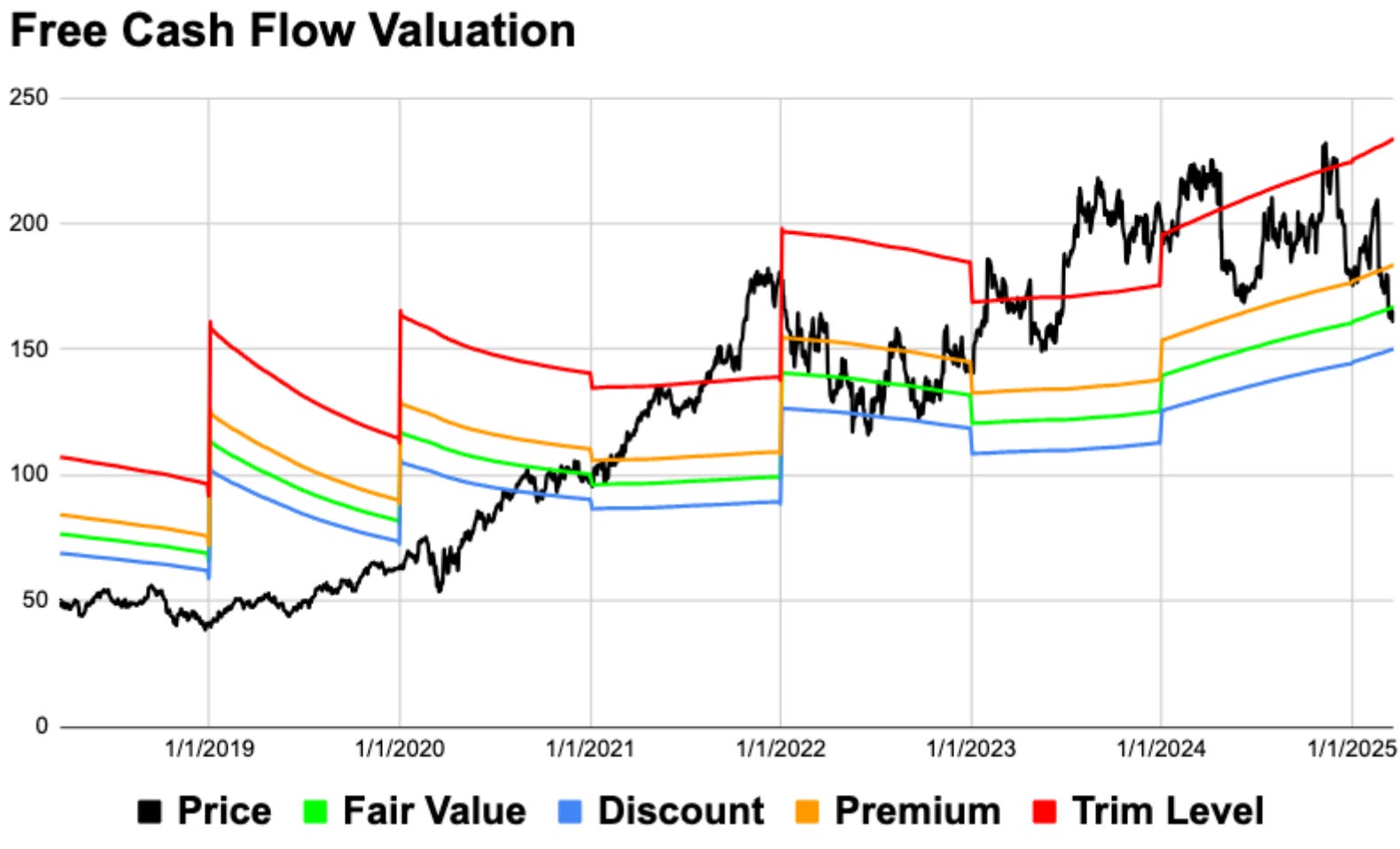

Based on the chart above, the company is currently trading at a fairly reasonable valuation, but it hasn’t always been that way. Going back to the beginning of the chart, the company spent much of its time trading for a deep discount before, during, and after the pandemic. Coming out of the pandemic the stock surged significantly in 2020 and 2021—54.8% and 84.1%, to be exact—which caused it to become drastically overvalued. The price dropped by about 20% in 2022, and the stock became more reasonably valued. However, in 2023 it was more of the same: a huge stock surge and an unreasonable valuation. In 2024, the stock price oscillated quite a bit before ending the year down 12.5%, which is where the stock would be today, had it not been for the recent market selloff.

The company has a solid long-term expected rate of return of 12.11% with the pieces of that estimate being a 0.68% dividend yield, a 0.20% return to fair value factor, and an expected earnings growth rate of 11.23%.

To sum up, ODFL 0.00%↑ has generated above-average market returns over the past decade, exceeding 20% annually. The recent revenue dip is something investors should pay attention to, but the GPM is expanding, and although the ROIC has dipped, it remains at a very healthy level. The dividend history is short, but with the company maintaining a low payout ratio, I don’t believe there is anything to fear in that regard. At the moment, I think the stock might be worth considering for dividend investors, and any price weakness in the future could present a great buying opportunity.

The long-term quality score for ODFL 0.00%↑ sits at 83.3%, while the 2024 is very similar at 82.4%. The biggest reason for both is the recent slide in revenue and the lack of dividend history.

If you found this content insightful consider upgrading to a paid subscription, you can see live valuation ratings here, at any time. Additionally, you’ll gain access to a live complimentary Free Cash Flow Valuation Tool for over 200 stocks, as well as access to our 3 model portfolios. The paid subscription is only $5 per month and you can cancel any time.

In case missed them, here are some recently covered stocks:

Moody’s Corporation MCO 0.00%↑

Also check out some tools to help with your investing journey

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin

My article will be soon

Mine will be coming out soon