Zoetis Inc. (ZTS)

")

ZTS 0.00%↑ is a global animal health company that offers a wide array of products including vaccines, medicines, diagnostics and other health-related servics. The company was originally a subsidiary of PFE 0.00%↑ but became its own independent company when it was spun-off in 2013. Zoetis is headquartered in Prasippany, New Jersey and currently employees approximately 13,000 people.

Below is a brief financial overview of some financial metrics:

Is ZTS a winner?

As mentioned above, ZTS 0.00%↑ has only been its own stand alone company for a little less than 12 years. During that time the company has done very well, in fact, 8 out of the past 10 years the company’s stock has had a return of no less than 12.17%. The only two down years were 2022 where the stock dropped nearly 40%, and thus far in 2024 the stock is down about 10%, with only a few weeks remaining. The total return since inception has been slightly higher than 500% resulting in a market-beating compound annual growth rate of 16.8%. Zoetis’ ability to beat the average market return over its short life is impressive and something investors should take note of.

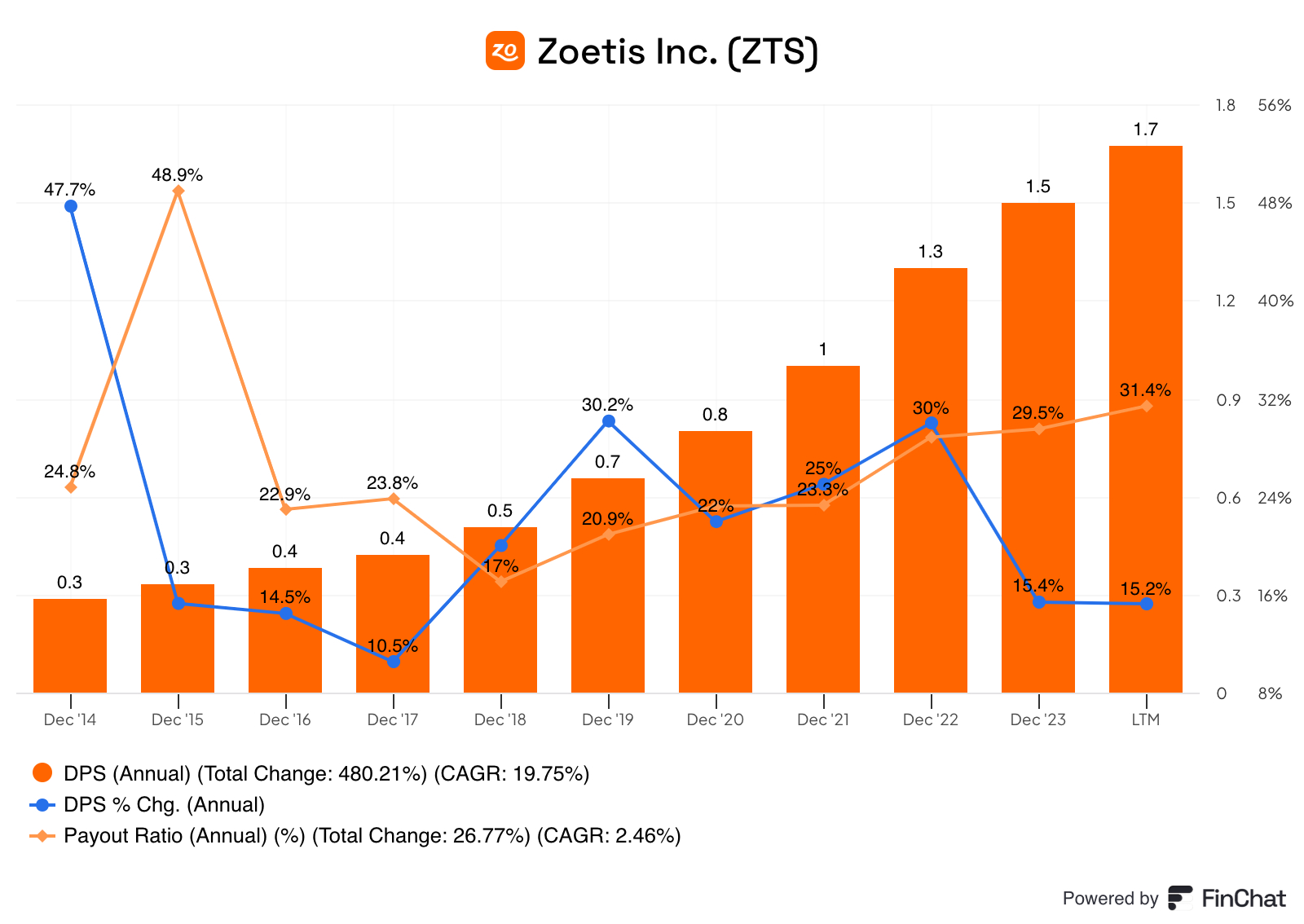

Dividend Data

Since we are looking for a quality Dividend company it’s only logical we examine the company’s dividend history.

ZTS 0.00%↑ is a dividend contender having paid and raised its dividend every year since inception. The company has a staggering 10-year dividend growth rate of nearly 20%, and the total overall change in the amount paid has gone up almost 5x. As you can see the company has always provided shareholders with fantastic increases given that on the chart below the lowest increase was 10.5% in FY 2017.

What’s even better about ZTS 0.00%↑ is that the payout ratio, aside from 2015, has been extremely low and even 2015 was still less than 50%. To be fair, the payout has been climbing since FY2018 but is still remarkably low which will allow for future dividend increases.

Clearly, this company has a generous dividend policy and has been rewarding its shareholders for all of its existence, and thus should be considered by dividend focused investors.

Quality Metrics

In my opinion, there are three important quantitative characteristics all high-quality businesses possess. These metrics are an increasing revenue stream, a steady gross profit margin and a healthy return on invested capital. Let’s explore these metrics for ZTS 0.00%↑ and see if it meets the standard for a high quality company.

The revenue per share metric has more than doubled over the past decade, climbing at a rate of about 8% per year. Aside from a less than 1% decline from 2014 to 2015, it has continued to rise every year since including a nearly 18% increase from FY20 to FY21. There isn’t a whole lot to say other than the company should continue to keep doing what it’s doing.

Zoetis’ gross profit margin has been steady and even improved some over the past decade. The GPM has increased at a clip of almost 1% per year, from a low of 64.7% in 2015 to north of 70% in the most recent fiscal year. Again, there isn’t much analysis needed, the company has a very robust gross profit margin and it’s been expanding.

The return on invested capital is final metric I want to discuss, and it has a similar path to the revenue per share and the GPM. The ROIC spent the first part of the past decade in the mid-teens before climbing to 22.5% in FY 2018. Since then the ROIC has remained above 20%, which is something I like to see from companies I own or may potentially own, and Zoetis does not disappoint here.

Obviously these metrics are very good, the company has been been able to consistently increase its revenue, while the GPM and ROIC are ever improving. In my opinion, ZTS 0.00%↑ is definitely a high quality business based on these metrics.

Valuation

The final piece of this puzzle is to determine if ZTS 0.00%↑ is trading for an attractive valuation. As the custom FCF valuation tool suggests, the stock is currently trading for a pretty significant discount to its fair value and is currently rated a “STRONG BUY”.

From the chart above we can surmise the company rarely traded for a significant discount relative to its free cash flow until 2024. In fact, 2018 was last time this stock traded at a discount for an extended period of time. Beginning in 2019 the stock began to climb, but the free cash flow didn’t follow as the FCF dipped by about 7% compared to 2018. Following a decline in the stock price in early 2020 the stock basically doubled by the end of 2021. However, 2022 is where ZTS 0.00%↑ took a beating with its FCF declining by more than 20% and the stock dropping by nearly 40%. In 2023, the stock recovered nicely, as did the FCF and thus the stock was reasonably valued all year with only minor fluctuations. In the most recent fiscal year the FCF surged almost 45% but the stock has declined almost 10% so far this year leading to the possible undervaluation.

ZTS 0.00%↑ currently has a long-term expected rate of return of about 14.5% and the pieces of that estimate are as follows:

A current dividend yield of 0.97%.

A return to fair value factor of 4.23%.

An expected growth rate of 9.29%.

In conclusion, ZTS 0.00%↑ is an exceptionally run company with amazing financial metrics. The company has consistently rewarded shareholders with robust dividend increases, well-above inflation. So far this year the market appears to have forgotten about ZTS 0.00%↑ as the stock has struggled, and now may be a good opportunity to for investors to consider this dividend contender.

If you found this content useful consider upgrading to a paid subscription. You’ll gain access to live valuations for the 50 stocks in our High Quality Dividend Growth Investable Universe, a complimentary Free Cash Flow Valuation Tool for over 200 stocks and access to our 3 model portfolios. The paid subscription is only $5 and you cancel any time.

In case you missed it, here are some recently covered stocks:

The Hershey Company HSY 0.00%↑

Lam Research Corporation LRCX 0.00%↑