Wingstop Inc. (WING)

")

Before we dive into WING 0.00%↑ , here are some recently covered stocks you may be interested in:

Intercontinental Exchange, Inc ICE 0.00%↑

Background

Wingstop Inc. WING 0.00%↑ is a fast-casual restaurant chain specializing in chicken wings and operates more than 2,500 locations worldwide, with about 98% of those locations being franchised.

The company is headquartered in Dallas, Texas and was founded in 1994.

WING 0.00%↑ has a current market cap of approximately $9.5B and over the past decade has a total return exceeding 1,400%, or a CAGR of more than 31%.

Quality Financial Metrics

Let’s take a look at some of Wingstop’s financial metrics and assess how the company has performed.

Revenue Per Share:

The RPS for WING 0.00%↑ has grown from $2.8 per share in 2015 to $21.4 just last year, a total increase of more than 650%, equating to a CAGR of 25.1%.

The “slowest” growth for WING 0.00%↑ occurred in 2021 where it still rose almost 13%, while its best year was 2024, rising more than 38%.

Overall there is strong growth, driven by the company’s expansion and operational innovations, including an AI-driven Smart Kitchen.

Gross Profit Margin:

The gross profit margin peaked at 71.5% in 2015 but has since dipped to less than 50% in recent years.

As with all restaurants, the company has faced increasing cost pressures including rising food and labor costs, despite Winstop’s rising revenue, this could indicate a potential challenge in maintaining profitability efficiency over time.

Return on Invested Capital:

WING 0.00%↑’s ROIC has climbed more than 200% since 2015, rising from just 13.9% in 2015 to more than 43% last fiscal year.

There’s been steady growth along the way, indicating improved efficiency in generating returns, likely as a result of its scalable franchise model and the aforementioned revenue growth.

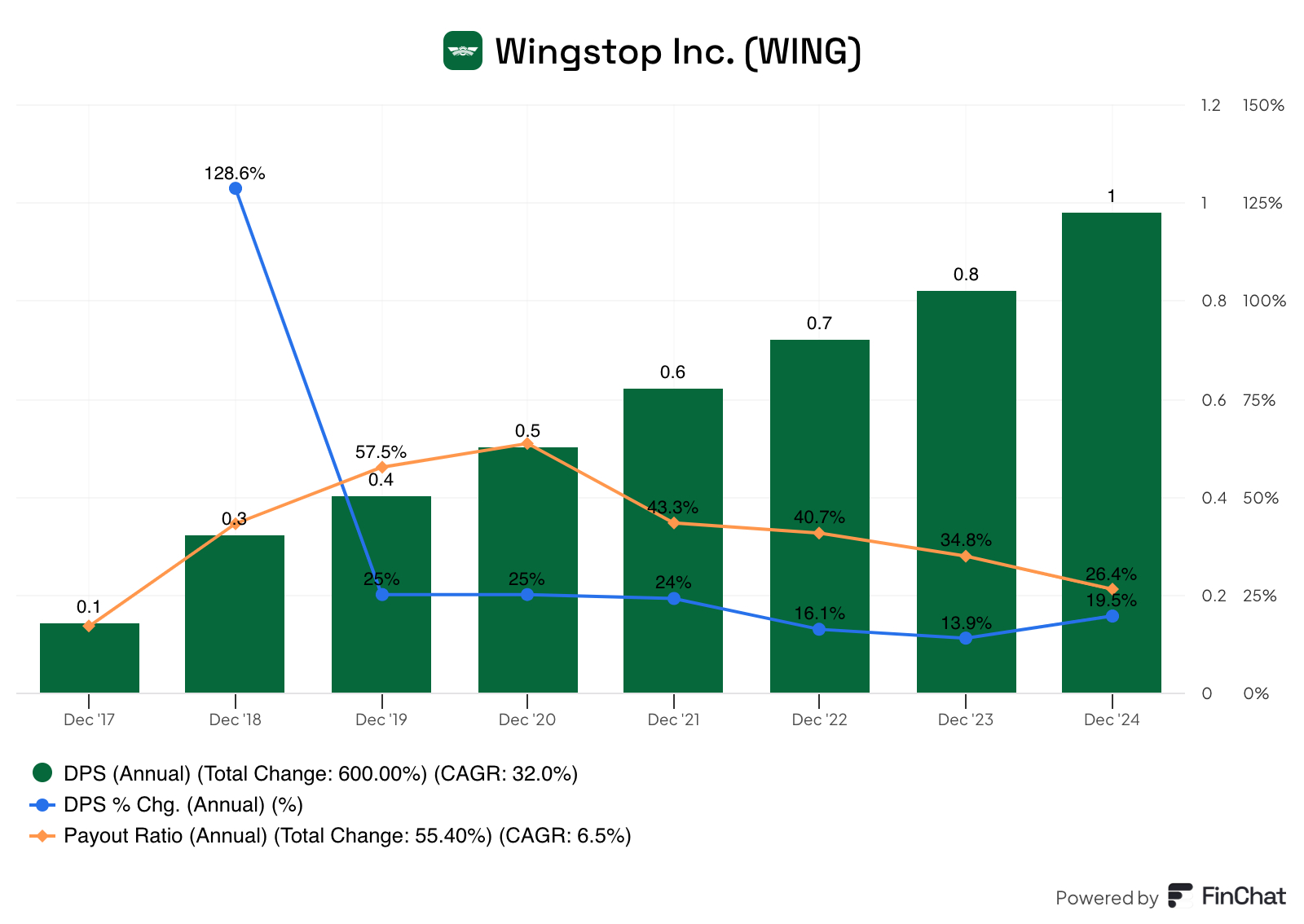

Dividend Data

Wingstop has paid a dividend for about 8 years, including some special dividends along the way.

The best part about catching a company paying dividends early on is the dividend growth. WING 0.00%↑’s 3-year dividend growth rate is 16.67%, while its 5-year DGR is even better, at 20.79%.

The payout ratio is incredibly low and should allow for dividend increases long into the future.

Potential Headwinds

Macroeconomic Pressures: There’s been a noticeable pullback in spending, particularly among lower/middle-income consumers, resulting in modest same-store sales growth of just 0.5% in Q1 2025. Additionally, management stated, they anticipate a mid-single-digit decline in same-store sales in Q2 2025 due to tough prior-year comparisons, reflecting broader economic challenges, such as inflation and reduced discretionary spending.

Increased Operational Costs/Margin Pressure: As mentioned above, the company’s GPM has been drifting slower, and despite efforts to stabilize food costs by diversifying into boneless chicken products, WING 0.00%↑ faces increased cost of sales, which grew to 76% of company-owned restaurant sales in Q1 2025 from 74.5% the previous year. Furthermore, SG&A expenses increased by $6.3M as a result of investments in growth and system implementation. These rising costs, coupled with a shrinking GPM, could be squeezing profitability.

Q1 2025 Earnings

Wingstop has a solid history of earnings, topping both EPS and Revenue estimates in 12 of the last 16 quarters.

In late April, WING 0.00%↑ announced Q1 2025 earnings with a double-beat, GAAP EPS was $3.24, blowing past expectations by $2.37 per share, on revenue of $171M which exceeded the consensus by $150K. Lastly, normalized EPS also beat expectations by $0.16, at $1.03 per share.

Total revenue (including franchise sales) was $1.3B, up 15% YoY. This increase was driven by 126 net new restaurant openings and 0.5% domestic same-store sales growth.

After increasing their store count by 126 net new locations, this brought their total to 2,689 locations globally. The company now expects net new global unit growth of 16% to 17% in fiscal 2025.

Net income for the quarter surged more than 220% to $92.3M.

Digital sales rose to 72% of total sales, indicating the strength of Wingstop’s delivery options, as well as the MyWingstop platform.

Adjusted EBITDA grew by 18.4% to $59.5M.

Valuation

Let’s take a look at our valuation chart and see if WING 0.00%↑ is undervalued at the moment.

Based on my custom FCF model, the stock appears overvalued by quite a bit, nearly 30%, with a current price of $349, and a fair price closer to $270. The stock is up 23% YTD, contributing to the overvaluation.

Forward Return Assumptions

As you know, I always look for a rate of return of at least 10%, and WING 0.00%↑ surpasses that threshold by a few a percentage points with a 14.25% expected RoR. Below is what makes up that estimate:

Dividend Yield: 0.31%

Return to Fair Value Factor: -5.22%

Expected Earnings Growth Rate: 19.17%

Final Thoughts

Wingstop has outpaced the broad market over the past decade by more than double. The company has some excellent financials, but the GPM margin has noticeably shrank over the past few years which may be cause for concern. The dividend history is short, but so far so good, great growth and a low payout ratio. Overall, everything about this company appears great, except the valuation Thus, I believe investors should wait for a pretty decent decline in the price before loading up on this dividend grower.

Also check out some tools to help with your investing journey:

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin