Intercontinental Exchange, Inc. (ICE)

Before we dive into ICE 0.00%↑, here are some recently covered stocks you may be interested in:

Lennox International LII 0.00%↑

Background

Intercontinental Exchange, Inc ICE 0.00%↑ is a global leader in financial market infrastructure, operating exchanges, clearing houses, and data services for equities, derivatives, commodities, and fixed income.

The company is headquartered in Atlanta, GA and was founded in 2000. Since then ICE has grown through numerous acquisitions, most notably the NYSE in 2013.

ICE has current market cap of about $85B and over the past decade has a total return exceeding 300%, equating to a CAGR of about 15.2%.

Quality Financial Metrics

Let’s examine some important financial metrics for Intercontinental Exchange and try to ascertain how the company has performed.

Revenue Per Share:

ICE 0.00%↑’s revenue per share has shown strong long-term growth, nearly tripling over the past decade, resulting in a CAGR of 11.6%.

The annual percentage change highlights volatility. The 2022 decline likely reflects a normalization after the prior two year surge.

Recently, there’s been a recovery, suggesting ICE 0.00%↑ has regained momentum, possibly driven by its increasingly diversified portfolio—i.e. data services, ESG products, but also robust trading volumes on exchanges like the NYSE.

Return on Invested Capital:

The highest ROIC was in 2017 at 3.0%, likely indicating improved operational performance (compared to other years) but still quite low.

The 2021-2022 period marks a low point, potentially tied to the 2021 revenue peak not translating to efficient capital returns.

Overall, ICE 0.00%↑’s ROIC has been very low, possibly implying that while the company generates strong revenue (as discussed above), its returns on invested capital are modest. This could be due to multiple factors including high CapEx, acquisitions, or clearing house operations which require significant upfront capital, but could take time to yield above-average returns.

Note: The gross profit margin is typically discussed here but was omitted because due to ICE’s business model, the costs of running exchanges and providing data are generally classified as operating expenses as opposed to COGS…this makes their GPM essentially 100% and not worthy of analyzing.

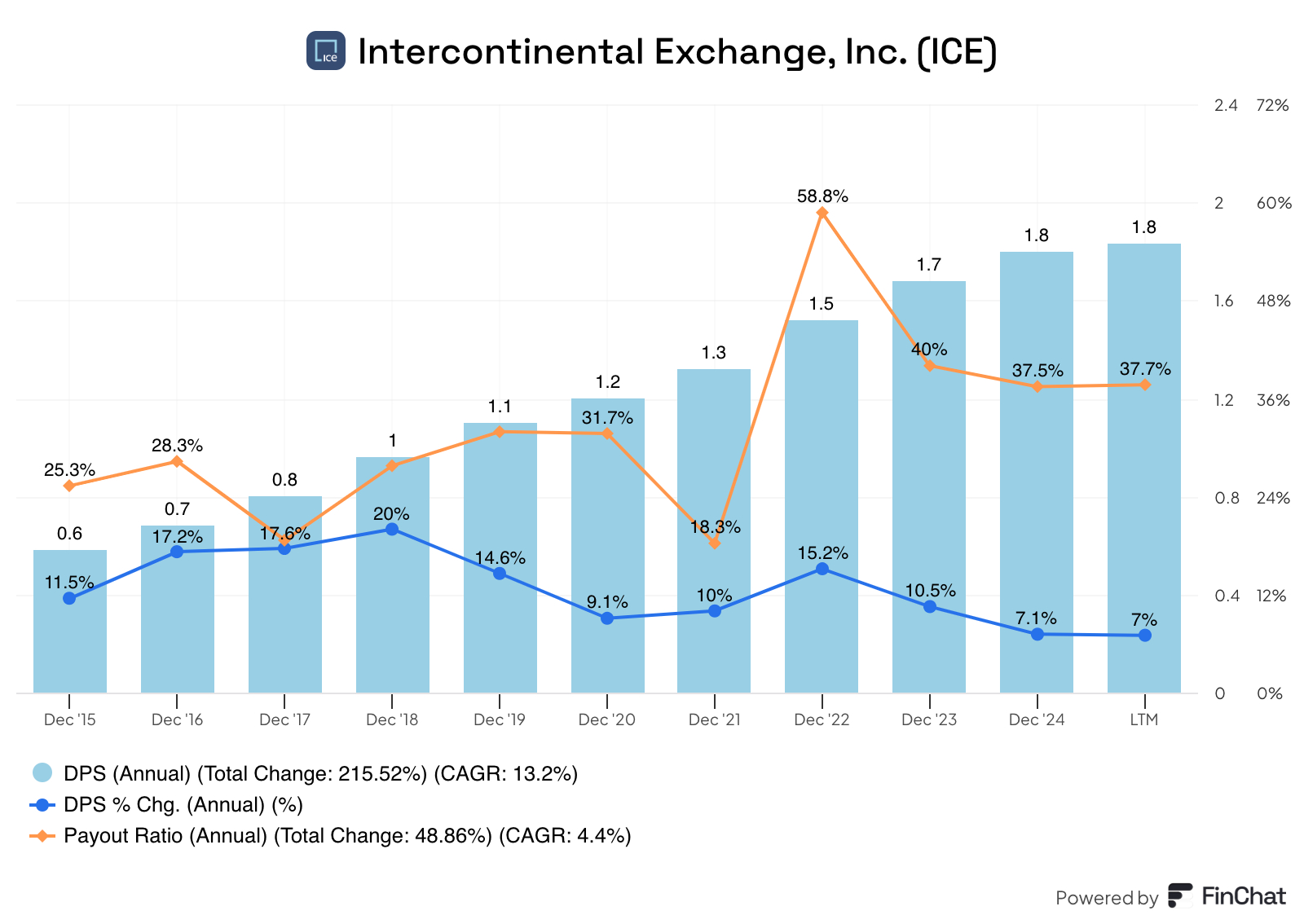

Source: FinChat.io Dividend Data

ICE 0.00%↑ has paid a dividend for a little more than 10 years.

The company’s 3 & 5-year dividend growth rates both exceed 10%, while its 10-year dividend growth rate exceeds 13%.

The payout ratio has been trending higher in recent years but is still low enough to allow for future dividend growth.

Source: FinChat.io Potential Headwinds

Regulatory Compliance: ICE 0.00%↑ operates in a highly regulated environment across multiple jurisdictions which poses significant challenges. Regulatory changes, such as Basel III Endgate and EMIR 3.0, could increase costs for clearinghouse operations and client clearing activities. Furthermore, oversight from bodies like the CFTC and FINRA adds complexity and operational expenses, especially as ICE expands into new markets and products like the recently acquired American Financial Exchange.

Mortgage Technology: ICE’s Mortgage Technology segment is facing headwinds as a result of macroeconomic factors like rising interested rates a cooling housing market. Recently, the April 2025 ICE Mortgage Monitor Report noted a slowdown in home price growth to 2.2%, signaling reduced activity in the housing sector. Also, higher interest rates have lowered prepayment rates (0.48% in January 2025, the lowest in almost a year) and increased delinquency rates (3.47%, up 10 bps YoY). These trends, coupled with natural disaster impacts (i.e. California wildfires), put a strain on the segment, which contributes 22% of ICE’s revenue.

Q1 2025 Earnings

ICE 0.00%↑ has a pretty good history of earnings, beating EPS estimates in 12 of the last 16 quarters (2 of the “misses” were in-line with the consensus), while revenue has surpassed expectations in 10 of the last 16 quarters.

ICE reported adjusted EPS of $1.72, beating estimates by $0.02, on revenue of $2.47B. GAAP EPS was $1.38 beating the consensus of $1.37.

The Exchanges segment lead the way with $1.4B in revenue, up 12% YoY, driven by strong trading volume in derivatives and NYSE equities., boasting a 76% adjusted operating margin.

Fixed Income and Data Services generated $596M in sales, up 5% YoY, with steady growth from data analytics and bond trading, though its 39% margin reflects increased costs.

Lastly, the Mortgage Technology segment struggled with $510M in revenue, flat YoY, posting a negative 5% GAAP margin (40% adjusted) due to a cooling housing market, coupled with higher interest rates, despite new client wins like United Wholesale Mortgage.

On Thursday, July 31, 2025, ICE is expected to announce Q2 2025 earnings. The consensus estimates suggest adjusted earnings per share of $1.74, with GAAP EPS of $1.39, on revenue of $2.5B.

Valuation

Let’s examine our valuation chart and see if ICE 0.00%↑ is attractively valued at this time.