The Hershey Company $HSY

")

HSY 0.00%↑ is one of the largest and most well-known chocolate manufacturers in the world. The company was founded by Milton S. Hershey in 1894 and is based in Hershey, PA. Although the company is more than 100 years old, it continues to expand, not only selling chocolate bars but it has moved into the salty snack business by acquiring numerous brands, such as Skinny Pop, DOT’s Pretzels and Pirate’s Booty.

Here is a brief overview of some financial metrics:

Is HSY a winner?

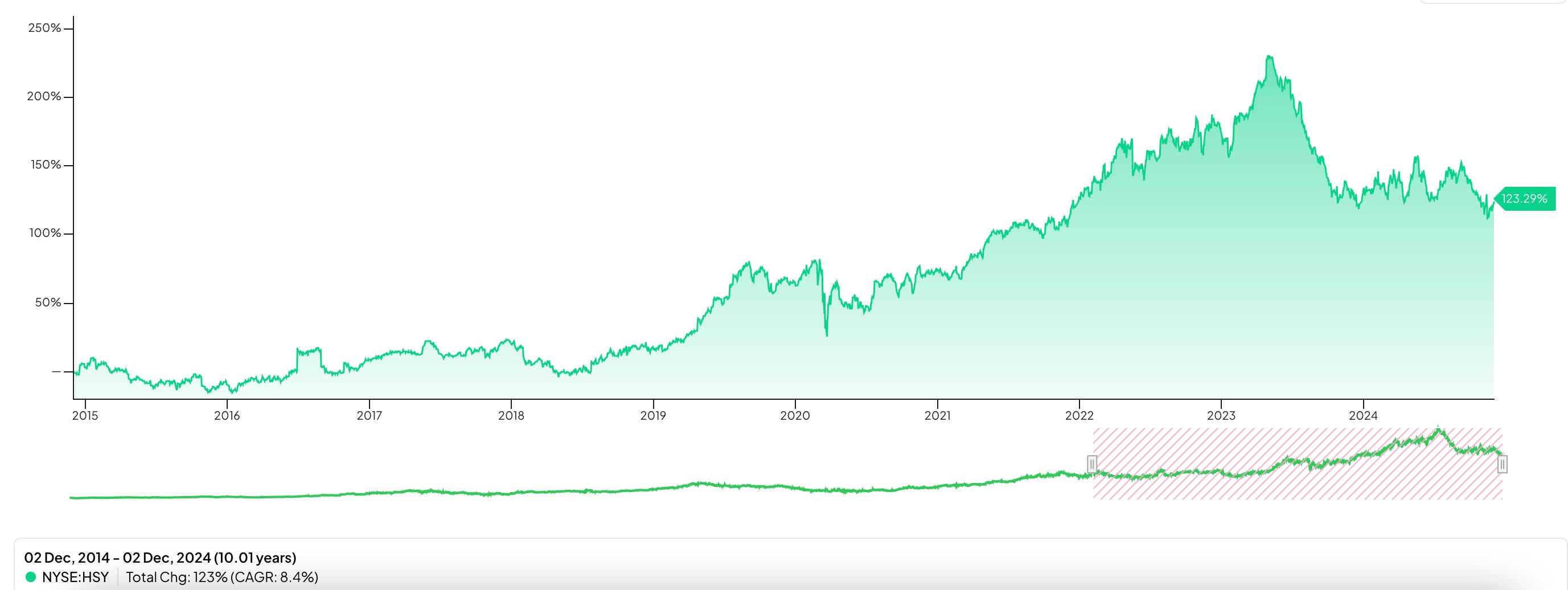

Since 1990 HSY 0.00%↑ has returned more than 4,000%, which equates to an annual total return of 11.4%, just below the average market return. Although HSY 0.00%↑ has not exceeded the standard market return, it has kept up pretty well over the long haul and in my view still a winner.

To be honest, Hershey’s growth has slowed more recently with an average total return of about 8.5% over the past decade. The stock has fluctuated quite a bit during that time with 4 down years (including 2024 thus far) and 6 up years. Beginning in 2015, the company saw a 12% decline, but followed it up with back to back years of double digit returns, 18% and 12% respectively. In 2018, there was a small loss of less than 3% but again the stock rose following a decline with a massive 40% increase in 2019 alone. The next years were all winners as well with the stock rising, 6%, 30% and 22% in consecutive years. Since then HSY 0.00%↑ has struggled with a nearly 18% decline last year and through November of this year the stock has dipped a modest 3.5%. The current rough patch the stock is in may be beneficial for potential investors but we’ll dive into the valuation a little bit later.

Dividend Data

Since we are looking for a quality Dividend stock it only makes sense we assess the company’s dividend history.

HSY 0.00%↑ is a dividend contender having increased its dividend for the past 14 years including a nearly 15% increase way back in February. This is actually better than the company’s 5 and 10-year dividend growth rates which sit at 12.88% and 10.29%. What’s even better is the 3-year DGR is just above 17%, which for dividend investors is a great sign the company is increasing their dividend at a bit faster rate. Overall, the dividend has risen almost 160% since FY 2014, while the payout ratio has decreased markedly leaving sufficient room for future dividend growth.

Quality Metrics

In my opinion, there are three important quantitative characteristics all high quality business should have, a rising revenue stream, a stable and consistent gross profit margin and a robust return on invested capital. Let’s review these metrics for HSY 0.00%↑ and see if it meets the standard for a high quality company.

As you can see early on in during the past decade, the revenue per share number was relatively stagnant with minimal growth over multiple years, which to be fair isn’t uncommon for such a mature company. However, since 2020 HSY 0.00%↑ has done a much more commendable job growing this metric with an increase of 11% from 2020 to 2021, followed by a nearly 17% increase from 2021 to 2022. This remarkable increase was due to gains from strong consumer demand as well as price increases implemented in the salty snack segment. It’s worth noting that while there was still a mid single digit gain in FY23 it was not as significant as the prior two fiscal years.

The gross profit for HSY 0.00%↑ has been quite steady with only minor fluctuations over the past decade. There was a small blip in FY 2016 & FY 2022 but other than this metric has been very stable which is what you would expect from a mature company.

Typically, I look for companies that have a return on invested capital of 20% or higher and HSY 0.00%↑ doesn’t disappoint. Since 2014 there’s only been two years where the ROIC dipped below 20% (2015 and 2016) but even so it was just a slight drop. Ultimately, I see no reason HSY 0.00%↑ would not be able to maintain a strong return on invested capital far into the future.

Overall, these metrics are very good, the revenue has begun increasing after an extended stagnant period, the gross profit margin is a thing of beauty, and the return on invested capital is healthy and stable. In examining these metrics for HSY 0.00%↑ I believe it to be a high quality company.

Valuation

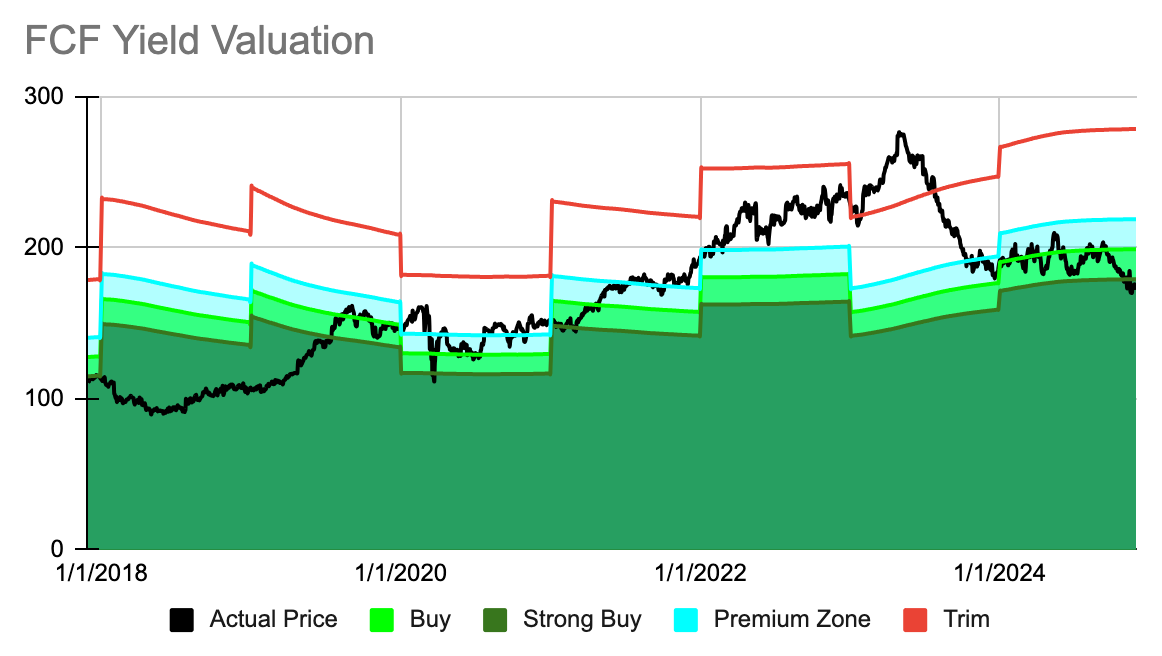

The last piece of the equation is to determine if HSY 0.00%↑ is trading for an attractive valuation and to do so we will look at it from a free cash flow perspective.

From the chart above you can see HSY 0.00%↑ has not traded for a real discount since late 2019. In fact, for basically all of 2018 and 2019 the stock was trading for a steep discount relative to its FCF. Throughout 2020 and 2021 the stock increased as the FCF did and the stock was trading for a fair valuation. In 2022 the stock continued to climb as did the FCF, just not at the same pace, thus leading to a significant overvaluation for most of 2022 and for much of 2023. Late last year the stock came back to reality due to the aforementioned 18% decline, as well as a 14% drop in FCF. Thus far in 2024 the stock has remained relatively flat but has dipped recently leading to it being rated a “buy” but is very close to a “strong buy”.

HSY 0.00%↑ has a current long-term expected rate of return of essentially flat, and the pieces of that estimate are as follows:

A dividend yield just north of 3%.

A return to fair value factor of 2.11%.

Projected EPS growth of -4.70%.

To sum up, HSY 0.00%↑ is trading for an approximate 11% discount to its fair value, the problem is I don’t see many potential growth prospects aside from a possible significant acquisition. Additionally, while HSY 0.00%↑ may be a good stock for someone looking for income, I typically want to see a higher expected rate of return and this just doesn’t provide it. This stock will remain on my watchlist and should its expected RoR rise in a material way, I will revisit it and see if its right for me.

In case you missed them, here are some recently covered stocks.

Lam Research Corporation LRCX 0.00%↑

Microsoft Corporation MSFT 0.00%↑