Microsoft Corporation (MSFT)

")

Microsoft Corporation is a multinational technology company known for its software products, hardware and services. Here are a few of the software products offered by Microsoft - Windows Operating System, Microsoft Office, Azure (cloud computing), SQL Server and Visual Studio. Microsoft’s popular touchscreen personal computers (PCs), tablets and the Xbox franchise are examples of their hardware products. Lastly, the services Microsoft offers are, Microsoft 365 which is a subscription based service offering access to Office Applications, cloud storage through OneDrive and team-building tools such as Teams.

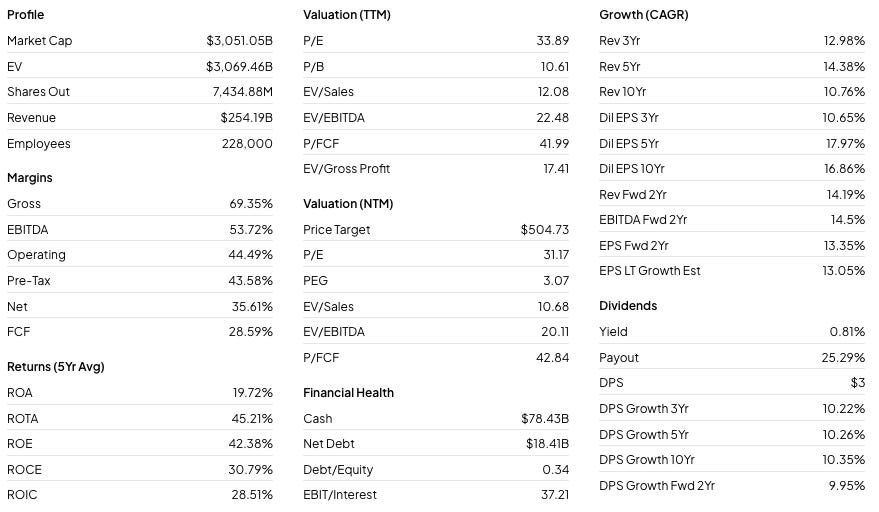

Here is a brief review of their financial metrics:

Is MSFT a winner?

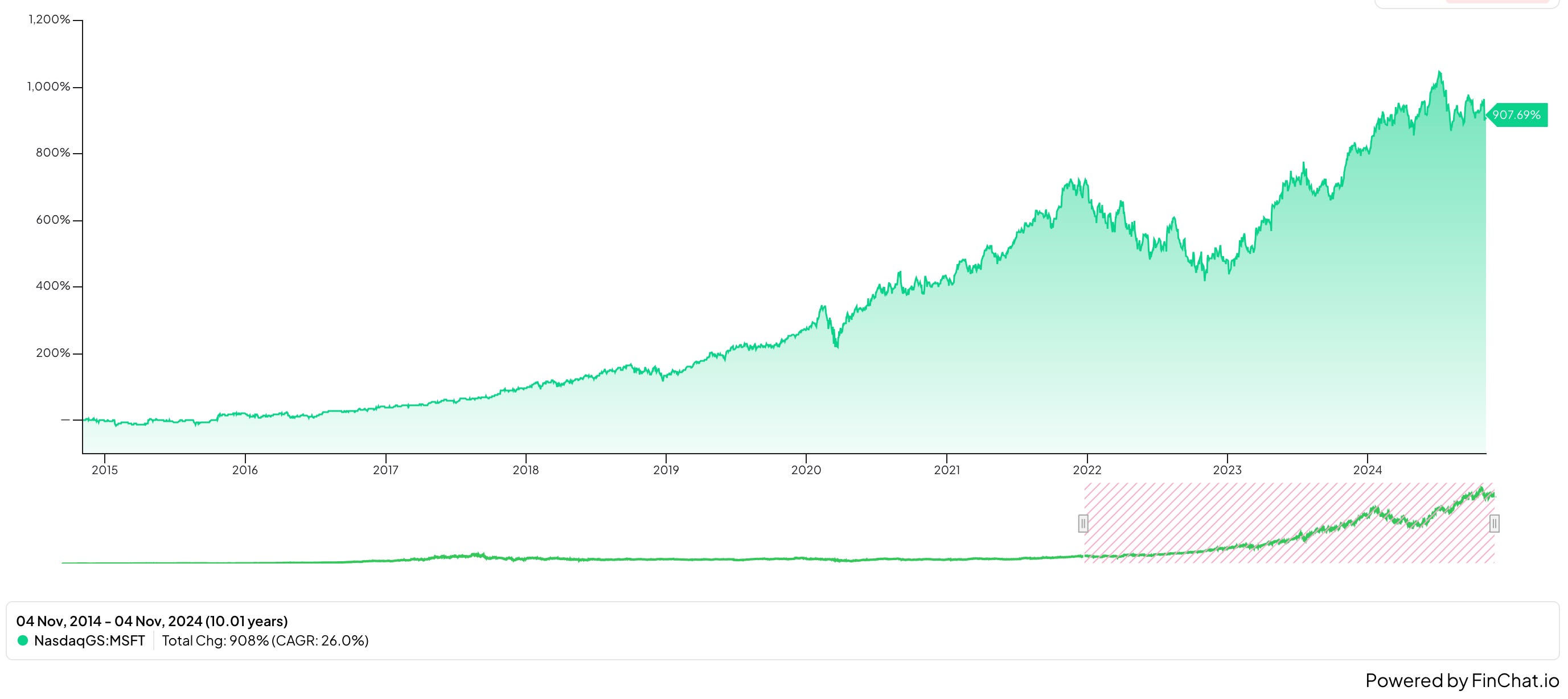

Since the beginning of 1990, or almost 35 years, Microsoft has returned a staggering 107,753%, or a market-beating total return of more than 22% annually. Microsoft’s ability to consistently provide investors with more than double the average annual return of the stock market makes it an obvious long-term winner.

More recently, Microsoft has given investors a whopping total return of 908% or 26% annually over the past decade. For comparison, during that same time period, the S&P 500 ETF (SPY) returned a very impressive almost 13% annually. This means while the market provided an exceptional return, MSFT was still able to return more than double during the same time frame. Clearly, Microsoft is a winner, consistently providing investors with reliable market beating returns, over the short and long term.

Dividend Data

Since we are looking for a quality Dividend stock it makes sense we examine the company’s dividend history.

MSFT has increased its dividend by nearly 150% over the past decade. This results in a compound annual growth rate of just over 10%. This 10% mark is in-line with its 3-, 5- and 10-year dividend growth rates which are all just above 10%. Additionally, in September of this year Microsoft raised its dividend 10.7% from $0.75 per quarter to $0.83 per quarter. All of this talk about increasing their dividend is very encouraging for any dividend investor. However, what makes all of this even better is that the company’s payout ratio has decreased significantly since FY 2015, dropping from 83% all the way down to 25% in FY 2024.

Microsoft’s ability to increase its dividend as well as maintain a low payout ratio is important to investors. This information can tell shareholders the company is in good financial health but is also committed to reinvesting in the business allowing for both dividend income in addition to capital appreciation.

Quality Metrics

In my opinion the three most important financial metrics that all high quality companies should have are an increasing revenue stream, a steady gross profit margin and a robust return on invested capital.

MSFT has nearly tripled its revenue per share over the past decade, rising from about $11.4/share in FY 2015 to $33 per share in FY 2024. This has come at an approximate annual growth rate of 12.5%. There’s no reason Microsoft should not continue to grow its revenue for the foreseeable future, given its market dominance.

The company’s gross profit margin is a thing of beauty, sitting anywhere between 65% and almost 70% over the past decade. Their ability to maintain and even improve this metric is admirable. This is because it’s not only a good indicator of profitability but also a company’s operational efficiency, such as effectively managing its costs and implementing a sound pricing structure.

The return on invested capital has fluctuated some over the past 10 years, but with the exception of 2018, every year’s ROIC has been 20.5% or higher. MSFT has shown a innate ability to generate healthy returns relative to its cost of capital and will likely continue to do so moving forward.

Recent Earnings

On Wednesday, October 30th Microsoft released FY 2025 Q1 earnings with a double beat - earnings per share came in at $3.30 (beat by $0.19) on revenue of $65.59B (beat by $1.03B).

Operating income increased 14% to $30.6 billion, while net income also rose 11% to $24.7 billion.

Revenue within the Productivity and Business Processes segment was $28.3 billion, up 12% versus the same time period a year ago. Some details about the areas within that segment are as follows:

Sales from Microsoft 365 Commercial products and cloud services rose 13% due to cloud revenue growth of 15%. Microsoft 365 consumer products and cloud services revenue gained 5% again mostly due to cloud revenue growth. The LinkedIn portion had revenue expand by 10%, and Dynamics products and cloud services grew by 14%.

Revenue from the Intelligent Cloud segment was up 20% to an outstanding $24.1 billion driven by Azure and additional cloud services revenue growth.

Sales from the Personal Computing division increased by 17% mostly as a result of the Activision acquisition.

Finally, Microsoft returned $9 billion to shareholders through a combination of dividends and share repurchases.

Overall the earnings report was not well-received by the market as the stock dropped approximately 5%. The entire earnings release can be viewed here.

Valuation

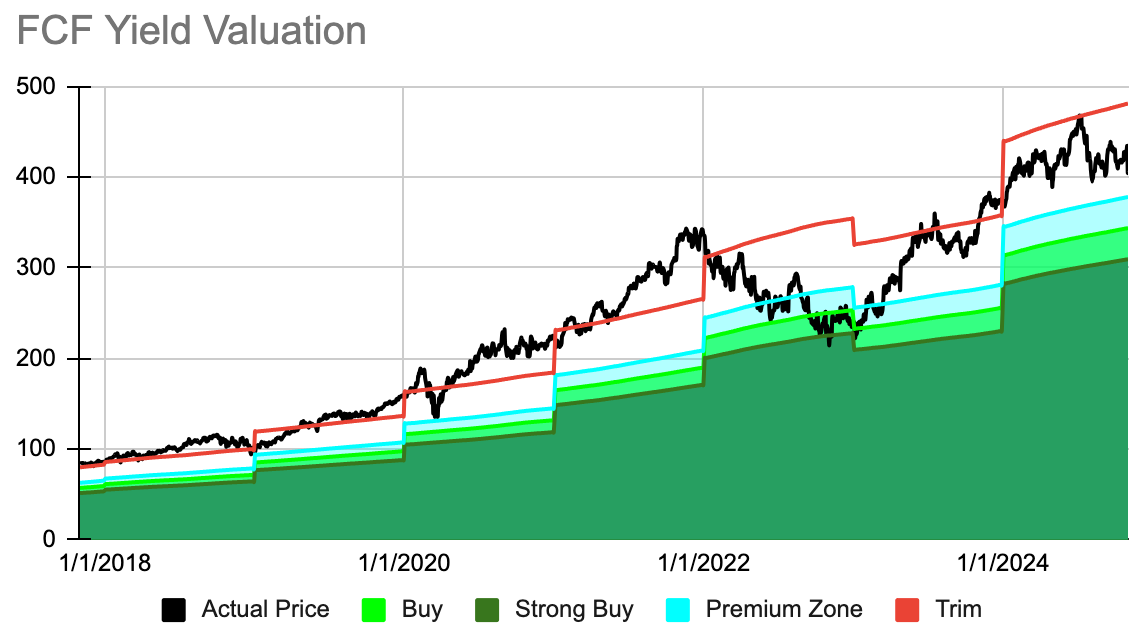

The final consideration we must examine is if Microsoft is trading for a reasonable price today. As the custom FCF valuation tool suggests, MSFT is trading a fairly significant premium to fair value and is currently rated a “HOLD”.

We can see from 2018 all the way through 2020 the stock traded at a premium relative to its free cash flow. Additionally, about midway through 2021 the stock became grossly overvalued and the stock dropped a little bit more than 28% during 2022. This drop provided investors with a very short-term opportunity to own a great company, as the stock climbed nearly 60% in 2023 and became overvalued again. Thus far, in 2024 the stock has again spent the entire time overvalued, even as its FCF/share increased by more than 20% from 2023.

MSFT currently has a long-term expected rate of return of 10.47% and the pieces of that puzzle are as follows:

A dividend yield of just 0.79%.

A return to fair value factor of -4.06%.

An expected earnings growth rate of 13.74%.

As we noted above, MSFT typically trades for a premium and the stock price tends to rise faster than its FCF. Since 2019, the company has had FCF/share growth of around 20% with an exception from 2022 to 2023 where it dropped a modest 8%. Microsoft has consistently increased its revenue per share over the past decade, and its gross profit margin and return on invested capital are both at healthy levels. In 2024, the stock has climbed about 8.5% and over the past year its rose nearly 15%. The valuation model suggests the stock is currently trading for a premium and investors may want to just monitor the stock and hope for a decent sized pullback.

If you find this content insightful you should consider upgrading to a paid subscription. You’ll gain access to live valuations for the 50 stocks in our High Quality Dividend Growth Investable Universe, a complimentary Free Cash Flow Valuation Tool and access to our 3 model portfolios. The paid subscription is only $5 and you can cancel at any time.

Quality At A Fair Price is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.