Allegion PLC (ALLE)

")

Allegion PLC is a global company which specializes in security products and solutions. More specifically the company focuses on locks, door hardware, access control systems, and additional security technologies. Allegion was created via a spin off in December 2013 from Ingersoll Rand Inc.

Here is a brief glance at their financial metrics:

Is ALLE a winner?

Since its spin off in late 2013, Allegion has a total return of 231% equating to a compound annual growth rate of 11.5%. This return is slightly above the long-term average of the market which is about 10%. Although this company has only been around a little more than a decade, and has performed well, it will be interesting to see if it can sustain its growth and remain a “winner”.

Dividend Data

Since we are looking for a quality dividend stock it’s only fitting that we consider the company’s dividend history.

ALLE has paid a dividend every full quarter since it split off from Ingersoll Rand. The company has grown its dividend at an exceptionally healthy rate over the past decade with its 10-year growth rate at 20%.

One thing a dividend investor likes more than a growing dividend, is a growing dividend coupled with a low payout ratio, and ALLE has not disappointed. As you can see from the chart below, ALLE has a very low payout ratio, with the highest on the chart only being 37.6%. The payout ratio has trickled up over the past 10 years but it is still at a very reasonable level to allow for the dividend to continue growing.

Quality Metrics

In my opinion the three most important financial metrics that all high quality companies should have are a growing revenue stream, a stable gross profit margin and a healthy return on invested capital.

Let’s examine the chart below to see how ALLE fairs with all of these metrics.

Allegion has nearly doubled its revenue per share over the past decade, climbing from $22 in fiscal 2014 to $41.5 in the most recent fiscal year, resulting in a CAGR of 7%. The company did see a slight decrease during the pandemic but has since continued to grow this metric quite nicely.

The gross profit margin has been incredibly steady with only minimal change during the past ten years. Allegion reached a high of 44.6% in fiscal 2017 and a low in fiscal 2022 of 37.2%. A company’s ability to earn predictable margins is imperative for investors to see as it usually means the company has effectively managed its pricing strategy leading to a strong competitive advantage in the market.

The final metric to examine is the return on invested capital. The ROIC, much like the gross profit margin, has overall been steady for Allegion. The company’s ROIC in 2014 was 18%, before rising to 26.5% in 2018. Since then it has trickled lower but was still a healthy 19.8% in fiscal 2023. A company’s ability to maintain a consistent ROIC is a sign of a strong business model and indicates the company can generate reliable returns regardless of economic conditions (like a pandemic).

Recent Earnings

On Thursday, October 24th Allegion released Q3 earnings with revenue of $967.1M (missed by $2.94M) and earnings per share of $2.16 (beat by $0.18).

The adjusted earnings per share were up 11.3% compared with the same time period a year ago where the company earned $1.94. Net earnings per share rose 12.4% to $1.99 from $1.77 in Q3 2023.

Revenue climbed 5.4% overall and 3.3% on an organic basis. The organic percentage excludes any acquisitions and divestitures, in addition to impacts from currency exchange rates. The rise in revenue was attributed mostly to volume growth.

Allegion was also able to increase its operating margin from 21% to 22%, while its adjusted operating margin also increased 100 bps, from 23.2% to 24.2%.

The company repurchased 300,000 shares during the quarter as well as paid a dividend of $0.48 per share.

Allegion reaffirmed its projected revenue growth for fiscal 2024 to between 2.5% to 3.5%, with organic revenue growth around 2%. Furthermore, the company raised its outlook for FY 2024 earnings per share to be between $6.70 and $6.80, or on an adjusted basis to be in the range of $7.35 to $7.45. The earnings report was surprisingly not received well by the market as the stock dropped about 4% following the release, which can be read here.

Valuation

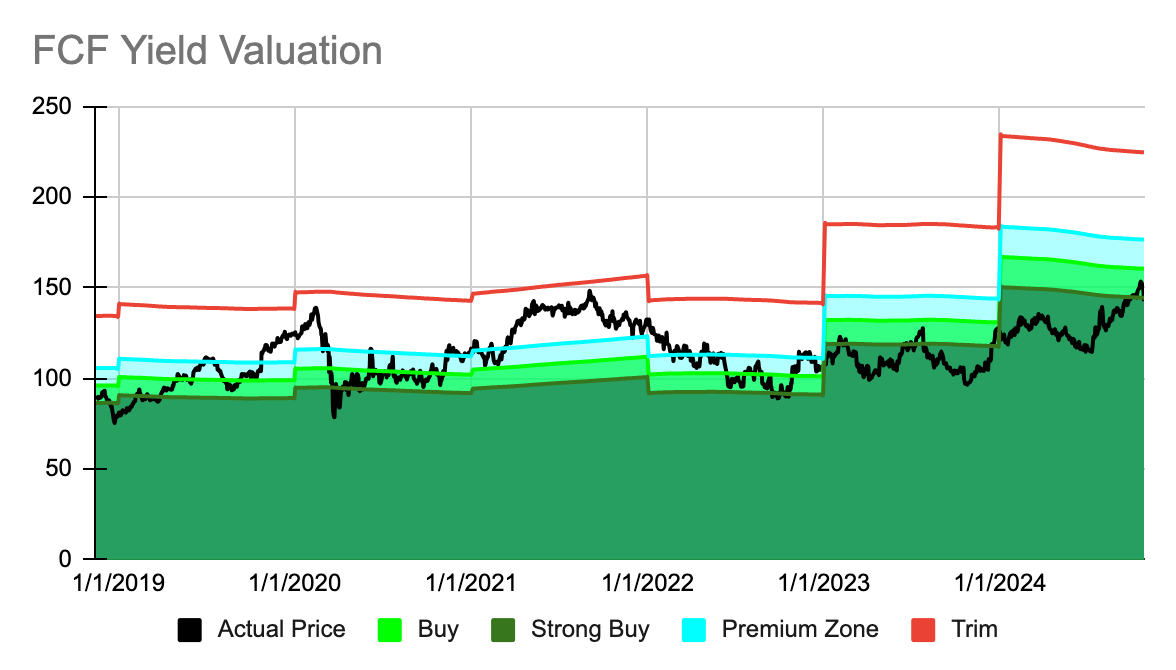

The last consideration we must evaluate is if Allegion is trading for a reasonable price today. As the custom FCF valuation tool suggests, ALLE is trading at a slight discount to fair value and currently sits in the “ STRONG BUY” zone. This rating changed following its recent earnings release and was mentioned in the “Valuation Rating Update” that was released earlier this week.

We can see in the first half of 2019 the stock was a buy; however, by very early 2020 the stock had become overvalued by quite a bit. Late in the first quarter of 2020 the stock dropped by almost 30% from nearly $130/share to around $85-$90 per share. For the remainder of 2020 the company was reasonably valued before another run up in share price in 2021, leaving the company overvalued again. Throughout most of 2023 the stock has been rated a “strong buy” by the valuation model. In 2024, the stock trended above its fair value zone, however, the updated FCF per share figure from the most recent earnings report has pushed the valuation zones higher, indicating that Allegion is once again trading for an attractive price.

ALLE currently has a long-term expected rate of return of 11.68% and the components that make this ROR are as follows:

A dividend yield of 1.35%

A return to fair value factor of 2.11%

An expected earnings growth rate of 8.22%

Allegion is once again trading for an attractive price following its most recent earnings report. The company saw its free cash flow per share climb by more than 30% from 2022 to 2023 and again increased by 27% from 2023 to 2024. Allegion has had impressive revenue per share growth as well as a steady profit margin and a consistent ROIC over the past decade. Finally, although the stock price has risen 12% year-to-date and about 45% over the past year, the valuation model suggests some potential additional upside and investors may want to monitor this stock for any price weakness.

If you found this post insightful and would like to receive more Dividend Stock reviews directly to your inbox, subscribe below!

In case you missed it, here are some of the recently covered stocks.

If you find this content insightful you should consider upgrading to a paid subscription. You’ll get access to live valuations for the 50 stocks in our High Quality Dividend Growth Investable Universe, a complimentary Free Cash Flow Valuation Tool and access to our 3 model portfolios. The paid subscription is only $5 and you can cancel at any time.

I hope you have a wonderful rest of your day.