HCA Healthcare Inc. (HCA)

")

HCA Healthcare, or Hospital Corporation of America, is one of the largest healthcare service providers in the United States, and operates numerous hospitals, outpatient facilities, and other healthcare services. It was founded in 1968 in Nashville, Tennessee, by Dr. Thomas Frist Sr., Dr. Thomas Frist Jr., and Jack C. Masante. Over the past 10 years HCA 0.00%↑ has achieved a total return of more than 17% annually, outpacing the S&P 500.

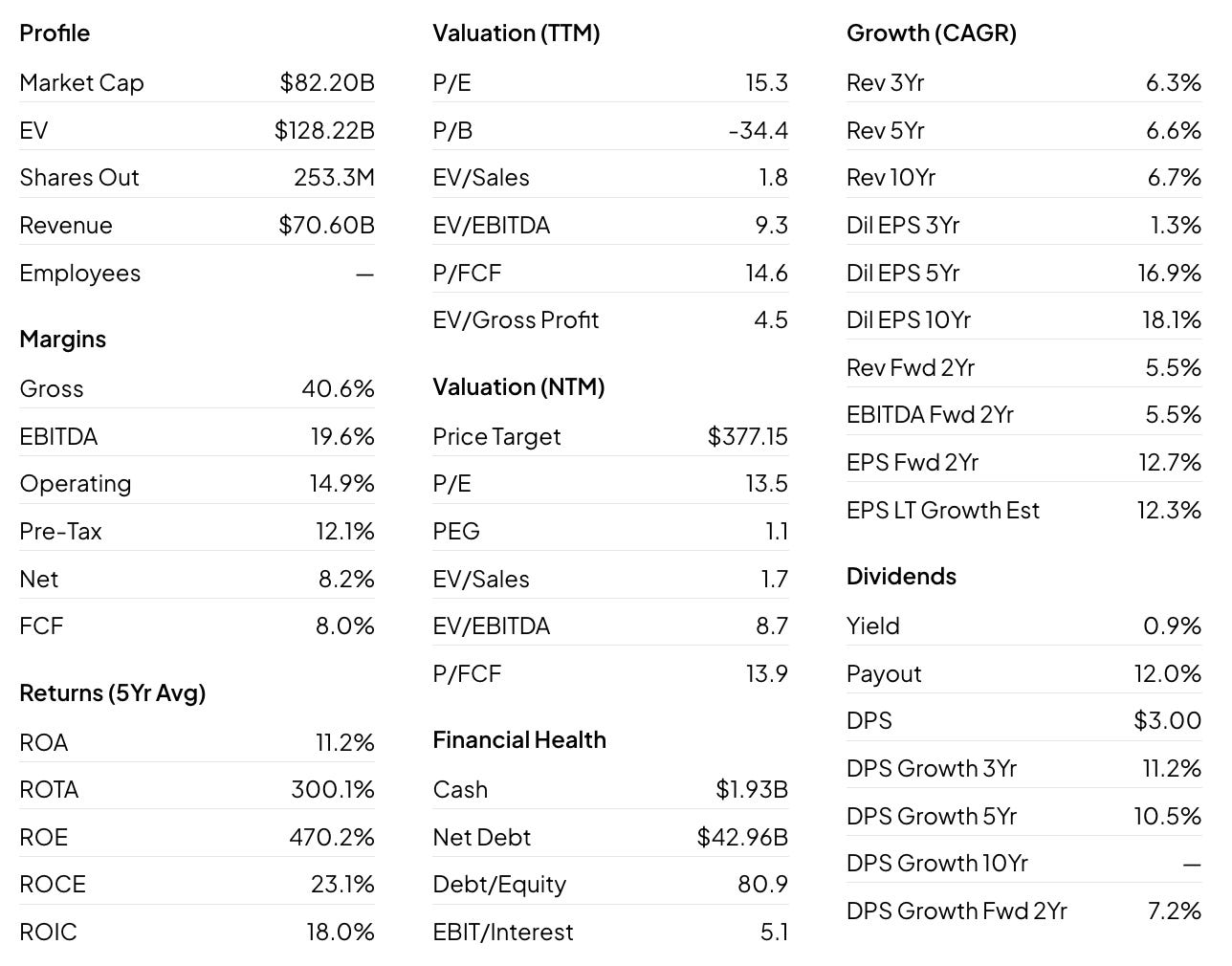

Additionally, below are some of the company’s current financial metrics:

Quality Metrics

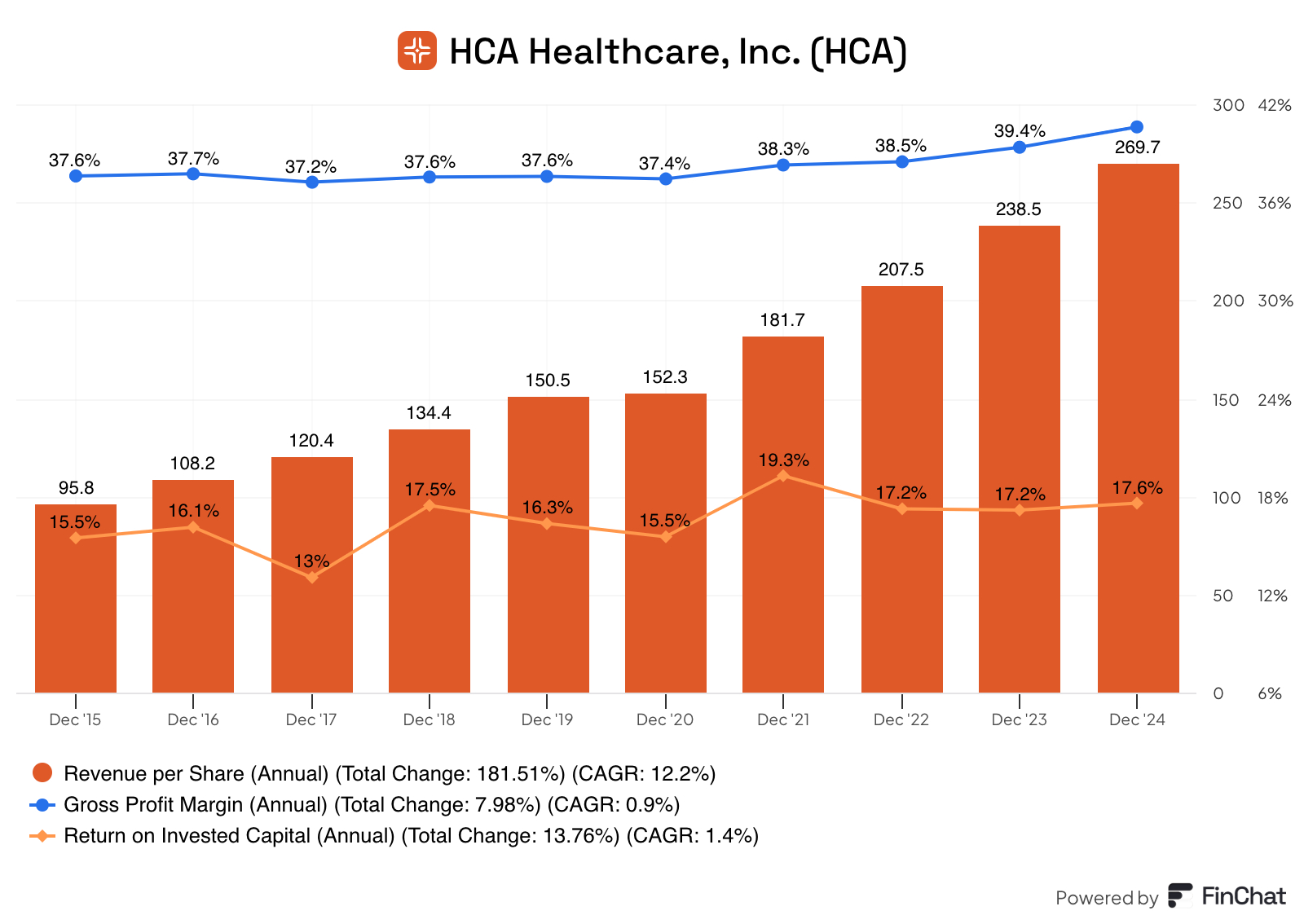

As you know, we like to examine three important financial metrics to determine if the company we are looking at is of high quality. Those financial measurements are revenue per share, the gross profit margin, and the return on invested capital. Let’s take a look at these and see how they measure up.

HCA 0.00%↑ has grown its revenue per share at a healthy rate over the past decade, more than 12% annually. This growth has occurred through a combination of actual revenue growth and share repurchases. I typically look at share repurchases when analyzing the company’s RPS, but usually, they don’t have a big effect. For HCA 0.00%↑, however, it’s a different story, and for some years more than others. From 2015 through 2017, the company averaged a 6% decline in total shares outstanding. From 2018 through 2020 there was minimal change, both positive and negative. However, in 2021 and 2022, the share count was reduced by 10% and 9.2%, respectively, which is a substantial amount considering I usually see less than 2% in either direction. Consequently, in a matter of just two years the share count was reduced by nearly 20%. FY 23 and 24 also saw a decent decline in share count but not nearly as much as the prior two years.

The company’s gross profit margin has remained steady over the past decade, with a noticeable rise from 2020 to 2024, climbing from 37.4% to 40.6%. A company’s ability to maintain and/or expand this metric is imperative, as it shows the company is efficient with its operations and also has a good pricing strategy companied with a high degree of cost control.

The return on invested capital metric, similar to the GPM, has expanded some over the years. Usually a 20% return on invested capital is what I like to see, and although HCA 0.00%↑ doesn’t ever surpass this mark, it does get close. Ideally, HCA 0.00%↑ can continually expand this metric and eclipse the 20% line in the very near future.

Overall these metrics are impressive and going in the right direction. The revenue per share is growing at a very solid rate, while the GPM and ROIC are both expanding. Based on this quantitative data is appears HCA 0.00%↑ is a quality company worthy of consideration from any dividend focused investor.

Dividend Data

HCA’s dividend history looks a little different due to the beginning of the pandemic where the company briefly discontinued paying a dividend for a few quarters. Prior to that, the company had initiated a dividend in 2018, and post 2020, it picked back up where it left off. As you can see, the dividend growth rate, marked by the blue line, has ranged from 7% to 17% (excluding the two outlying years), and the payout ratio has been quite low enough, even with the dividend increases. Although the history is short, it appears the company is trying to establish a dividend policy that will reward shareholders with consistent dividend increases. This remains to be seen for the time-being but will be something to monitor for the future.

Potential Headwinds

As with any company, there are always challenges they face, and these can come from any direction-and HCA 0.00%↑ is no different. However, I believe the healthcare industry is uniquely vulnerable, especially now, with the cost of insurance skyrocketing on a yearly basis and companies not covering procedures or medications people think hospitals and insurance companies should cover. In addition, hospitals/medical facilities are one of the few, if not the only, places where the customer or patient doesn’t know what they will pay until after the service(s) are complete, in every other instance, you typically know the cost of the good or service you are purchasing prior to the transaction. This could put HCA 0.00%↑ in a bad position should they receive negative publicity from such an instance occurring at one or more of their hospitals.

Another issue facing companies in the healthcare space is regulatory compliance and maintaining clear billing practices. In fact, around 2001, the company settled a civil lawsuit in which they were accused of defrauding Medicare and Medicaid, along with other federal programs, through kickbacks and inflating costs, the company was ordered to pay a civil settlement of $745 million along with a criminal fine of $95 million. HCA 0.00%↑ appears to have corrected their practices over the past 20 years, since that incident but it may give investors pause should any inkling of such a scandal arise again.

The final issue I would like to bring up is something the company is currently dealing with, the natural disasters that occurred in 2024, specifically Hurricanes Helene and Milton. The company has stated that they incurred additional expenses and lost revenues totaling more than $250M in 2024 alone. While this obviously isn’t going to put a company like HCA 0.00%↑ out of business, who had 2024 revenues of more than $70B, they can have an effect on projects the company wanted to complete as well as lingering effects on overall revenue due to damage to buildings and systems.

2024 Q4 Earnings and Full-Year 2024

A few weeks ago HCA 0.00%↑ announced Q4 2024 earnings beating on both top-line revenue and bottom-line EPS. We’ll start with the latter which came in at $6.22 per share, beating estimates by $0.08 on revenue of $18.29B, topping expectations by $60M and climbing 5.7% from the same period a year ago.

Net income for the quarter was $1.438B a decrease from the prior year which was $1.607B. These numbers were slightly impacted from the sales of facilities in both 2024 and 2023.

For fiscal 2024 total revenues were more than $70B, about 10% increase from the same period a year ago. While EPS rose from $18.97 in 2023 to an even $22.00 in 2024.

The company also announced a 9% dividend increase in concert with the earnings release, raising the dividend from $0.66 per quarter to $0.72.

Overall the earnings call was well-received by the market with shares rising about 4% in the following day. However, since then the stock has lagged and essentially returned to where it traded pre-earnings at around $312 per share.

The full earnings release can be read here.

Valuation

The final piece of this puzzle is to determine if HCA 0.00%↑ is trading for an attractive valuation and to do so we’ll look at it from a free cash flow perspective.

During 2018 and 2019 the company traded at a slight premium to its fair value. As with many companies, that all changed when the pandemic hit; however, for HCA 0.00%↑ the FCF was impacted in a positive way, nearly doubling from 2019 to 2020. This would’ve been an ideal time to buy in to HCA 0.00%↑, but at that time no one knew what was going to happen, and of course hindsight is always 20/20. Coming out of the pandemic the company saw its stock price surge almost 60% in 2021 alone, leading to it becoming grossly overvalued. The decline in FCF in 2021 didn’t help either and the FCF dipped again 2022, where the stock declined, but only minimally, about 5%. Since then the stock has had some modest gains over the past two years, rising 13% and 11%, respectively, with the FCF climbing at a little faster pace. Thus far, in 2025, the stock has done well rising about 10%, even after taking into account the decline post their Q4 earnings.

HCA 0.00%↑ has a long-term expected rate of return of a little less than 10% and the components of that estimate are as follows: a 0.82% dividend yield, a -3.71% return to fair value factor as indicated by the overvaluation on the chart above, along with projected EPS growth of a little more than 12%.

Ultimately, the stock is rated as a HOLD given the overvaluation at the moment, by about 20%. Although the stock has done well historically it appears to be somewhat pricey at the moment and investors may want to wait for pullback before considering this dividend growth stock.

The long-term quality score for HCA 0.00%↑ comes in at 87.8%, while its 2024 quality score sits at 100%.

If you found this content insightful consider upgrading to a paid subscription, you can see the live valuation ratings here, at any time. Additionally, you’ll gain access to a live complimentary Free Cash Flow Valuation Tool for over 200 stocks, as well as access to our 3 model portfolios. The paid subscription is only $5 per month and you can cancel any time.

In case you missed them, here are some recently covered stocks:

Texas Roadhouse Inc. TXRH 0.00%↑

Follow Other Social Media Platforms

Link to Youtube

Link to X @LongacresFin