Cintas Corporation (CTAS)

")

Cintas Corporation CTAS 0.00%↑ provides a wide range of products and services related to business uniforms, facilities services and safety. The company is best know for its uniform rental programs, but its services also extend to first aid and safety supplies, fire protection, floor mats, and document shredding. Cintas plays a pivotal role in helping businesses maintain professional appearances and meet safety and regulatory standards.

Below are some the company’s financial metrics:

Is Cintas a winner?

Since 2015, CTAS 0.00%↑ has not had a losing year. In fact, the worst year for the stock was 2022 where it returned 2.96%, and its best was 2019 where it surged a whopping 61%. Even more impressive is the stock has returned at least 25% in 7 out of the last 10 years. Furthermore, on average the stock has returned more than 26% annually, which is more than double that of SPY 0.00%↑. Cintas’ ability to consistently beat the average market return, and do so handily, is a testament to the company overall and makes it a winner.

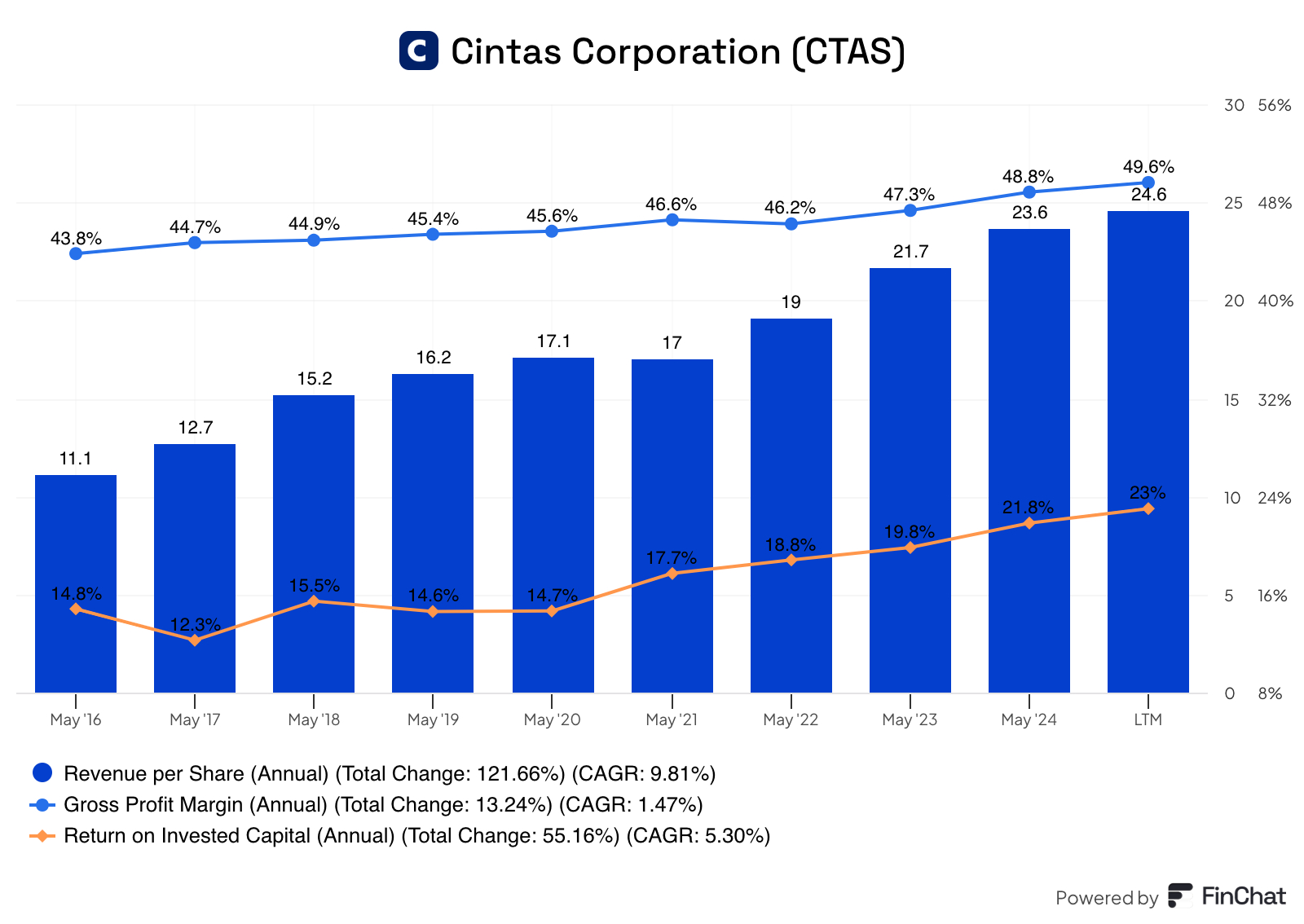

Quality Metrics

In my opinion, there are three important quantitative characteristics all high-quality business should possess. These are a growing revenue stream, a stable or expanding profit margin and a healthy return on invested capital. Let’s take a look at these metrics for CTAS 0.00%↑ and see how they measure up.

Cintas’ revenue per share has grown at a solid pace over the past decade, at nearly 10%. There were a couple very good years early on in 2016 and 2017 with increases of 14.4% and 19.8% respectively. This metric flattened out some during Covid, with a small decrease of less than 1% from 2020 to 2021. However, soon after CTAS 0.00%↑ was able to pick up where it left off with increases in and around 10% over the past 3 fiscal years.

There isn’t much to analyze about the company’s gross profit margin. This metric has been steadily increasing each year since 2016, reaching almost 50% over the last twelve months. Cintas should to continue to do what they’ve been doing and executing on their strategies.

Similar to the gross profit margin, the return on invested capital has gradually been increasing too. To be fair, there were some ups and downs early on over the past decade but overall increasing. And finally, since 2019 the company has been able to improve this metric too, starting at 14.6% and rising up to nearly 22% in fiscal year 2024.

There isn’t much to harp on regarding the company’s financial metrics. The company has an ever-increasing revenue per share metric, and the GPM and ROIC have been getting better and better. As mentioned above, the company should continue to operate as they have been and it’ll remain a high quality business.

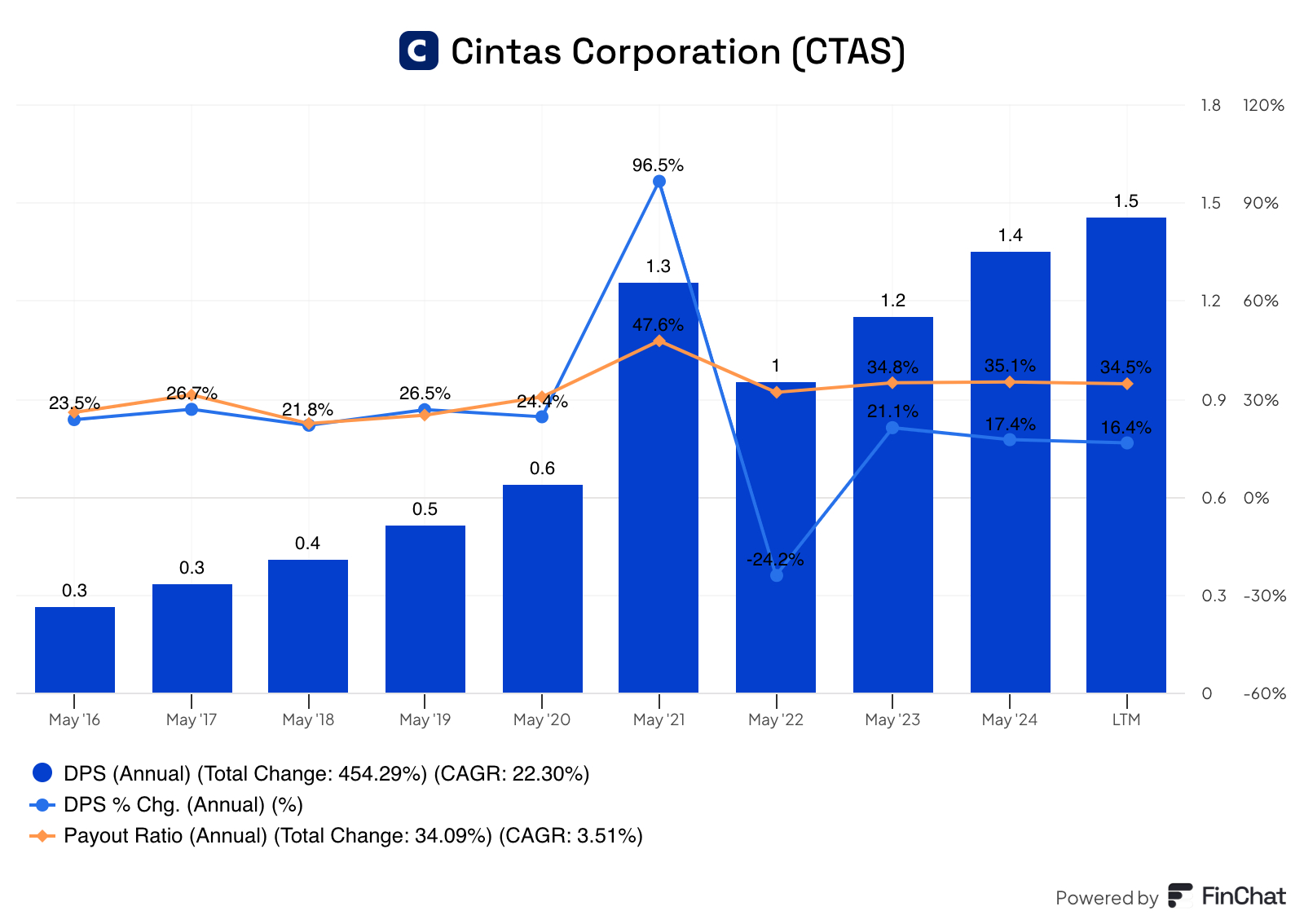

Dividend Data

Since we are looking for a quality Dividend company it’s only logical we investigate a company’s dividend history.

So the chart below looks a little strange because the company changed its dividend policy in late 2020 which effected the 2021 dividends. The company previously paid an annual dividend only but as of 2021, CTAS 0.00%↑ moved to quarterly dividends. No need to fret though, the company has a fantastic history of paying and growing its dividend for more than 40 years!

In fact, the company’s 3-, 5- and 10-year dividend growth rates are all near or above 20%, not too shabby for a company with a 40 year history of increasing their dividend. The one knock with CTAS 0.00%↑ is for investors who are only income focused, the stock yields less than 1%. Personally, I like to a combination of dividend growth and price appreciation and Cintas doesn’t disappoint.

The final positive here is the payout ratio is still very low, although it has trickled up recently. The first half of the past decade the payout ratio was closer to 25%, and since then has hovered closer to 35%. Although the payout has increased some, so there is a plenty of room for the company to provide shareholders with robust dividend growth.

Recent Earnings

Earlier in this month, CTAS 0.00%↑ announced Q2 2025 earnings with a beat on GAAP EPS which came in $0.07 above analyst expectations at $1.09 per share, on revenue of $2.56B which was in-line with estimates but was also a 7.8% increase from the prior year.

The company’s gross margin rose by 11.8% from the same quarter a year ago to $1.28B. The GPM for the quarter was 49.8%, a 180 basis point increase from FY 2024, primarily driven by lower costs for gasoline, natural gas and electricity.

The operating income also surged 18.4% to $591.4M compared to $499.7M for the same quarter last year. Additionally, the operating margin increased more than 2% to 23.1% for the quarter.

Management also provided updated 2025 guidance, with revenue expected to be between $10.255 and $10.32 billion (the previous low point was $10.22). Moreover, diluted EPS was also raised from $4.17 to $4.25 to a range of $4.28 to $4.34.

Naturally with the solid growth numbers and all the financial measures seemingly heading the right direction, the stock market responded with a huge sell off and the stock dropping by approximately 8%.

The full earnings release can be read here.

Valuation

The last piece of this puzzle is to determine if CTAS 0.00%↑ is trading for an attractive valuation. As the custom FCF valuation tool suggests, the stock is trading for a decent premium to its fair value.

From the chart above you can see CTAS 0.00%↑ typically trades for premium to its fair value, with the last time the company was trading for a significant discount was when Covid hit in early 2020. That dip was short lived, as the stock rose for the rest of the year and finished in the reasonable premium zone. In 2021, the stock began to climb as did the FCF but not by nearly enough to keep up, as the stock rose 26% and the FCF just 13.5%. The company spent most of 2022 near the reasonable value zone due to the stock price not changing much and the FCF only increased 8%. However, 2023 is a different story, with the stock surging almost 35% and the FCF actually dipping less than 1% leading to the valuation reaching the Trim zone by year-end. In FY 2024 the FCF rocketed up more than 50%, as did the stock price, but since the stock was already overvalued going into 2024, it led to it being grossly overvalued, until its most recent earnings report mentioned above.

Ultimately, the stock is rated a hold and is trading for an approximate 20% premium. The company has a long-term expected rate of return just below 10% and the pieces of that estimate are below:

A current dividend yield of 0.85%.

A return to fair value factor of -3.71%.

An expected earnings growth rate of 12.00.

In conclusion, CTAS 0.00%↑ is a wonderful company that has consistently topped the average market return and has not had a down year over the past decade. The financial metrics are all very good and even getting expanding too. The dividend yield is weak but what it lacks in yield, it more than makes up for with dividend growth and price appreciation. The recent earnings report was good but the stock did drop pretty significantly. A company like Cintas doesn’t appear to sell for bargain very much, so this is definitely worth monitoring for any future price weakness.

The quality score for Cintas is an excellent 95% making it one of the highest rated stocks in this investable universe.

If you found this content useful consider upgrading to a paid subscription. You’ll gain access to a live complimentary Free Cash Flow Valuation Tool for over 200 stocks as well as access to our 3 model portfolios. The paid subscription is only $5 and you can cancel any time.