Broadridge Financial Solutions (BR)

It's still cheap!

Intro

Beginning today we’re going to start revisiting some companies we’ve covered before and take a look at their recent earnings report to see which way the company is trending. Also, we’ll examine the valuation and compare it to the last time I covered it.

Broadridge Financial Solutions

The first stock we’re going to look at is Broadridge Financial Solutions, which was originally covered on 9/19/24. Since the original post BR 0.00%↑ has a total return (dividends included) of 9.14%. This includes accounting for the nearly 6% drop today due to their Q3 2025 earnings report…speaking of their earnings report, let’s dive into it.

The company had GAAP EPS of $2.05 per share resulting in a 15% increase from the prior year. Additionally, Non-GAAP EPS came in at $2.44, beating estimates by $0.03 on revenue of $1.81B, which represented a 4.6% increase YoY, but missed the consensus by $50M.

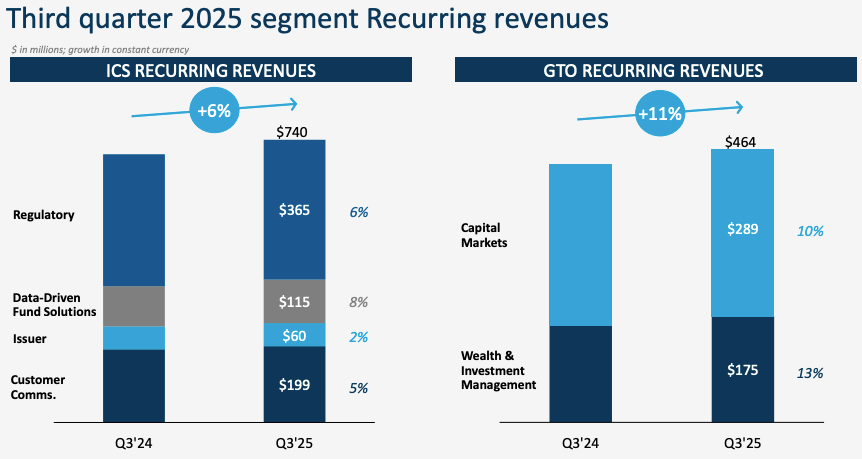

Revenue

BR 0.00%↑ has two reportable segments, Investor Communication Solutions and Global Technology and Operations.

The majority of revenue BR 0.00%↑ earns is Recurring revenue, which grew by more than 6% under the Investor Communications Solutions segment. Net New Business contributed 4% to that increase, while Internal growth made up the rest. Conversely, Event-driven (see below) revenue was impacted the most, declining more than 20% to $52.7M, due to lower proxy activity. Distribution (see below) revenues rose 4% as a result of higher postage costs but was offset by lower mail volumes.

Moving on to Global Technology & Operations, which only consists of Recurring revenues, this segment had double-digit growth in both arms of the segment. Capital Markets sales were $289M, a 10% increase, and was the result of higher software license revenue as well as elevated trading volumes. The increase for Wealth and Investment Management was 13%, to $175M, and occurred mostly due to the acquisition of Kyndryl’s Securities Industry Services.

Other Financial Measures

Operating Income rose nearly 14% to $344.9M for the quarter from $302.9M

Adjusted Operating Income increase almost 10% to a little more than $405M.

Operating margin increase 150 bps to 19%, while the adjusted operating margin expanded 100 bps to 22.4%.

2025 Guidance

Lastly, management reaffirmed their previously announced 2025 guidance, which is shown below.

Valuation

The last consideration, as always, is if the company is trading for an attractive valuation. Taking a peak at the original BR 0.00%↑ write-up, the stock was trading for a 15% discount based on the FCF valuation, with an expected rate of return of 16.32%. Currently, based on my model the stock is now 23% undervalued after today’s sell-off, with the new RoR coming in at 15.53%, and the pieces of that estimate as follows:

1.54% dividend yield

4.23% return to fair value factor

9.76% expected earnings growth rate

Final Thoughts

Broadridge Financial Solutions is a resilient business, with more than 94% of its total revenue being recurring. The company is making acquisitions where necessary, and although it wasn’t discussed here, the dividend has been growing at a robust rate, with its 10-year CAGR at almost 14%. The stock appears to be more undervalued than before, and thus, dividend investors may want to consider BR 0.00%↑ for their portfolio.

Also, let me know what you think of this new format. Is looking back on companies previously covered beneficial to you?

Also check out some tools to help with your investing journey

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin

thank you, I find everything interesting and look forward to every post