Allison Transmission Holdings (ALSN)

")

Allison Transmission Holdings, Inc. is a leading company focused on designing and manufacturing propulsion solutions for commercial and defense vehicles. Based in Indianapolis, Indiana, it’s the world’s largest producer of fully automatic transmissions for medium- and heavy-duty commercial vehicles. Founded in 1915 by James A. Allison, the company has a long history rooted in innovation, starting with its early ties to the Indianapolis Motor Speedway and evolving into a major player in vehicle technology. Over the past decade ALSN 0.00%↑ has returned essentially the market average, slightly more than 12% per year.

Additionally, here are some of the Allison’s current financial metrics:

Quality Metrics

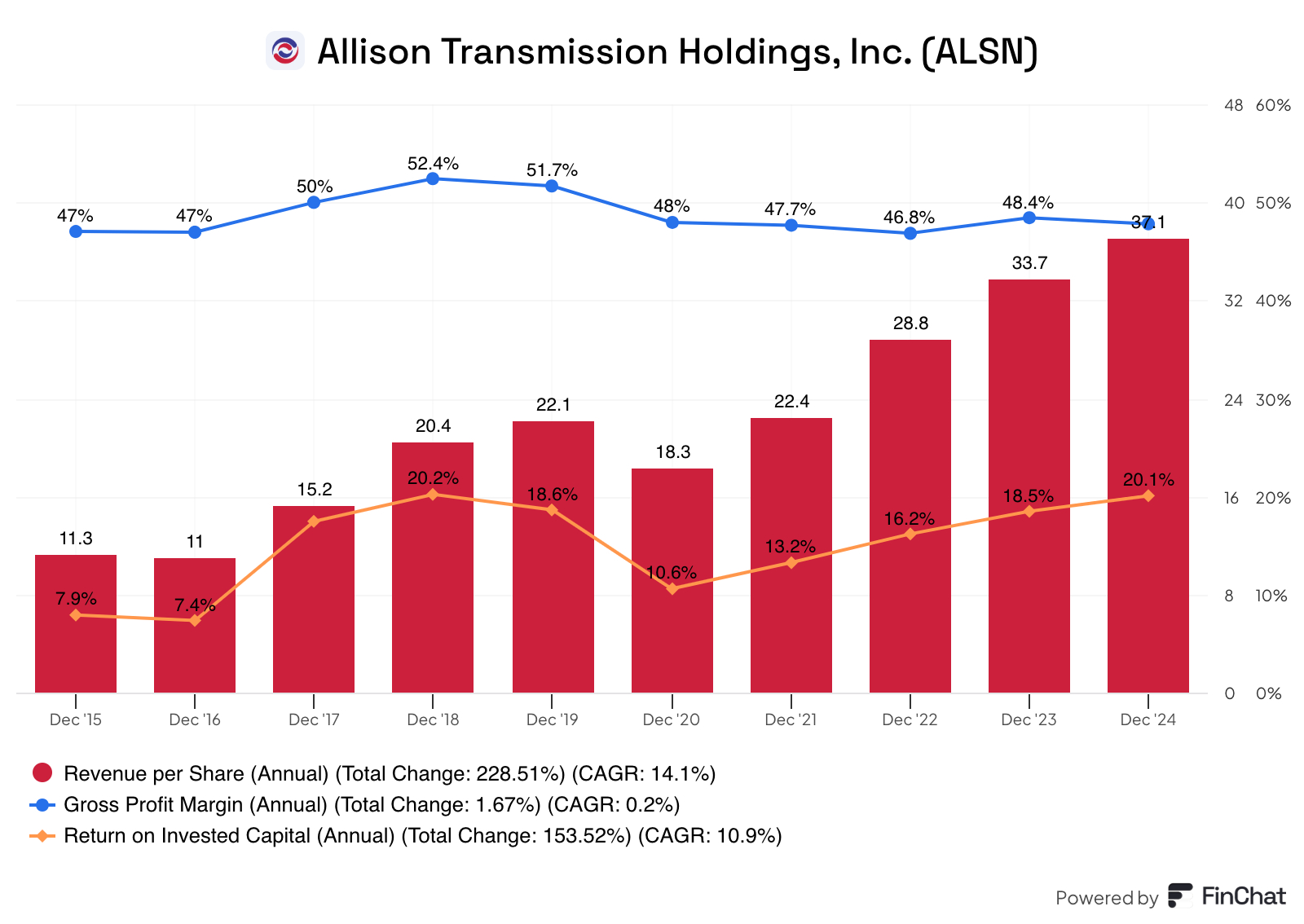

As I’m sure most of you know by now, I examine three financial metrics that are vitally important in determining if a company is of high quality. Those criteria are the company’s revenue per share, the gross profit margin and the return on invested capital. Let’s take a deeper look at these and see how they stack up.

Beginning in 2016, there was slight decline in the RPS metric; however, soon after this metric began to grow nicely. Over the next two fiscal years the RPS grew 38.6% and 34.4% respectively. ALSN 0.00%↑ saw another decent increase in 2019 of about 8.5% before the pandemic hit and there was a steep decline of 17.5%. Since then Allison has done a tremendous job increasing their RPS through a combination of growing revenue but also share repurchases. In 2021 and 2022 revenue surged more than 15%, but ALSN 0.00%↑ also reduced their share count by nearly 20% during the same time period. The most recent two fiscal years have also seen solid revenue growth of 9.6% and 6.3% respectively, all while the total share count was reduced by 4.5% and 2.1%.

There’s not much to analyze regarding the company’s gross profit margin. It’s been very stable, fluctuating only minimally, with a chart low of 46.8% in FY 2022 and a high of 52.4% in FY 2018. ALSN 0.00%↑ should continue to do what it’s been doing as they’ve been very successful at maintaining their margins over the past ten years.

The return on invested capital has oscillated a bit more than the gross profit margin. In 2015 and 2016 this metric came in around 7.5% in both years before shooting up to a minimum of 17.5% over the next three years, before the covid effect happened and it was basically cut in half. Since 2020 though this metric has been climbing at a healthy rate, back to pre-pandemic levels.

Overall, ALSN 0.00%↑ has some very good financial metrics, the revenue per share is growing at a nice rate through a combination of sales increases and a reduction in share count. While the gross profit margin has been very steady and the ROIC has recovered from the pandemic. Taking all of this into account, I think ALSN 0.00%↑ is a very high-quality business worthy of consideration from any dividend investor.

Dividend Data

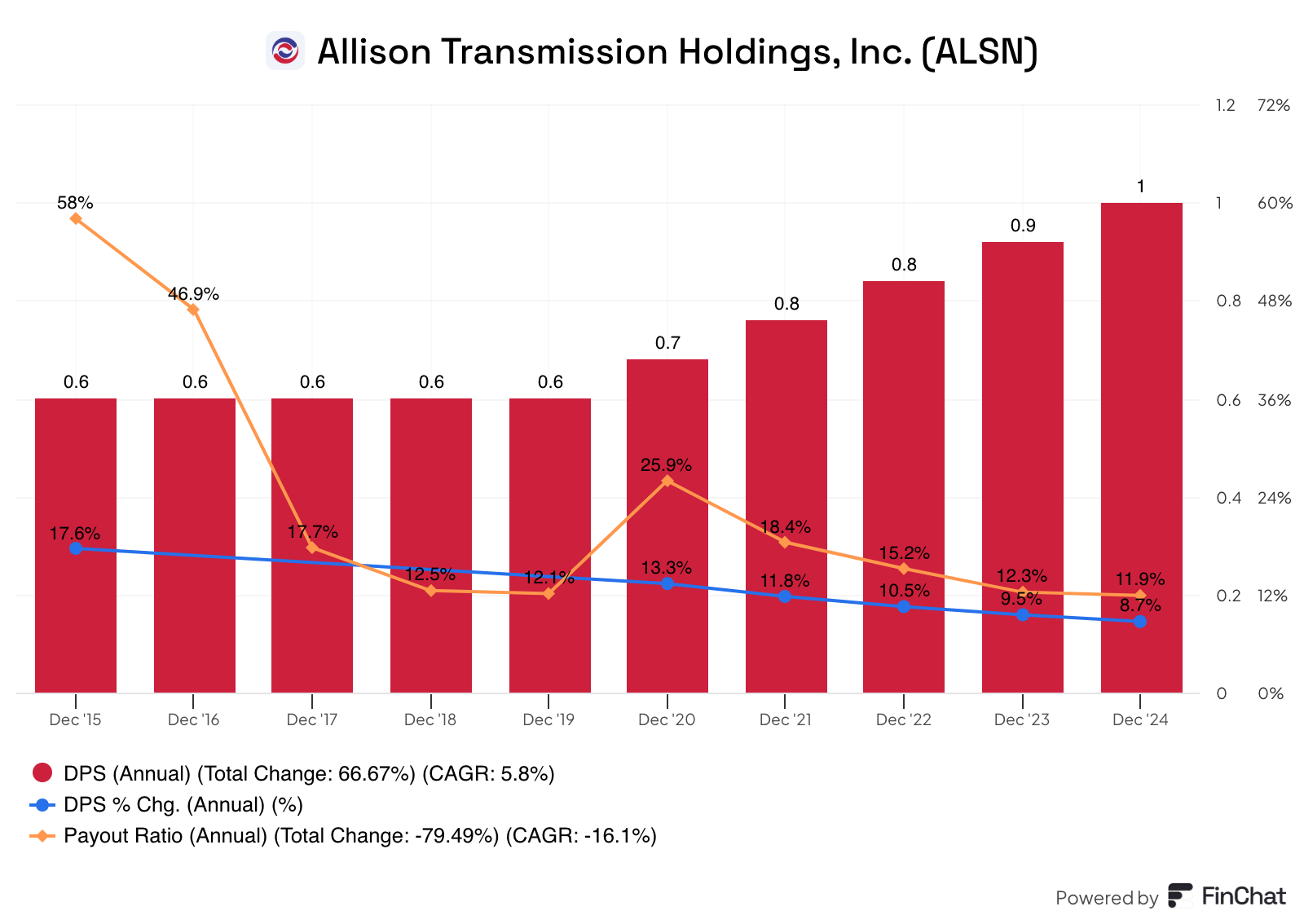

Allison Transmission has a short history of dividend growth…prior to 2020 the last time the company hiked its dividend was 2014, going from $0.12 per quarter to $0.15. Since 2020 though ALSN 0.00%↑ appears to now be a consistent dividend grower with its 3 and 5-year dividend growth rates at 9.6% and 10.8% respectively. The rate of dividend growth has been increasing, including an 8% increase announced just last week, all while the payout ratio is decreasing, an obvious great sign. In fact, the payout ratio for ALSN 0.00%↑ went from a high in 2015 of 58%, to a low in the most recent fiscal year of less than 12%, leaving ample room for future dividend growth.

Potential Headwinds

While Allison Transmission has a strong brand reputation and continues to see increased demand for its Class 8 Vocational vehicles as well as a surge in its Defense segment, the company still has challenges that may effect it in the future.

As with any company that deals with trucks and related vehicles, emissions are a big issue. The reason for this is that they typically use diesel which emits more harmful emissions than regular cars. Compliance with ever-changing emission standards from local, city and state governments can be cumbersome and sometimes unreasonable to attain. ALSN 0.00%↑ will need to continue to invest research and development to keep up with these constantly changing standards.

Another potential issue is the cost of acquisitions and the price paid by the acquiring company. In 2019, ALSN 0.00%↑ purchased two small companies, Vantage Power and AxleTech which have both been excellent at producing electric powertrains, but it’s imperative for ALSN 0.00%↑ to avoid overpaying for inferior companies or acquiring a company too far removed from their core line of business.

The final headwind I want to mention kind of goes without saying but I feel like it’s important to discuss. A variety of end-markets use Allison transmissions, so the company needs to maintain a high standard of production to avoid potential problems with their brand and reputation. Any type of significant or even moderate issue could cause them to lose customers and have financial problems for an extended period of time.

2024 Q4 & Full Year Earnings with 2025 Guidance

A couple weeks back, ALSN 0.00%↑ announced their Q4 2024 earnings with a double beat. Top line revenue was $796M, an increase of about 2.7%, and also beat estimates by more than $6M. While GAAP EPS was $2.01 for the quarter which exceeded expectations by $0.10 per share.

The sales increase in Q4 can be attributed to a couple different factors. The first is a 10% increase in net sales for their North America On-Highway segment, mostly driven by demand for their Class 8 vocational vehicles and price increases on a variety of products. Another contributor to the increase was a 5% increase in sales of service parts and support equipment with price increases again being the main driver. The last reason was an 8% increase in their Defense end market with their Tracked Vehicle applications being the primary reason. All of these increases were offset by a modest increase manufacturing expenses for the quarter.

Net income for the quarter was $175M, resulting in the aforementioned diluted EPS of $2.01. Also, adjusted EBITDA for Q4 came in at $270M, while adjusted FCF for the quarter was $136M.

Full-Year 2024 sales were $3.2B a 6.2% rise from FY 2023 and the components of that increase are similar to the ones mentioned above for Q4. Net income for FY24 was $731M with diluted EPS of $8.31.

Management also provided 2025 guidance which came in weaker than analysts expected causing a 10% drop in after-hours trading. ALSN 0.00%↑ expects revenue of $3.2 to $3.3 billion, with net income in the range of $735M to $785M, and adjusted EBITDA around $1.2B.

The full earnings call can be read/listened to here.

Valuation

The final piece of this equation is to determine if ALSN 0.00%↑ is trading for a reasonable valuation and to do so we’ll look at it from a free cash flow perspective.

Beginning in 2018 the company was undervalued and it continued that way for 2019 as well. ALSN 0.00%↑ saw a big dip in FCF during 2020, with it dropping by about 30%. Since then the company’s FCF has gradually increased with some years better than others; however, even though it’s been increasing the run-up in this stock during 2023 and 2024 where it rose 42% and 88%, respectively has led to it becoming grossly overvalued.

The company has an expected rate of return of just 2.47% mostly due to the overvaluation. The pieces of that calculation are a dividend yield of about 1%, a return to fair value factor of -7.26%, and an expected EPS growth rate of 8.74%.

Overall, ALSN 0.00%↑ has kept up with market returns and has solid financials all headed in the right direction. The dividend growth history has been short, but the company has been fairly consistent with its increases since 2020 and I see no reason their dividend growth shouldn’t continue. There are some potential headwinds to consider but nothing the company can’t manage. Obviously, the biggest knock on ALSN 0.00%↑ is the valuation, the stock has climbed too high, too fast and is clearly overvalued at this time. Consequently, investors should probably wait for a large pullback before considering adding to or initiating a position.

The long term quality score for ALSN 0.00%↑ comes in at 88.2% with its revenue, GPM and FCF being the main drivers for the high score, while its dividend history is the biggest lag. Additionally the 2024 quality score for ALSN 0.00%↑ comes in at a very impressive 95%.

If you found this content insightful consider upgrading to a paid subscription, you can see the live valuation ratings here, at any time. Additionally, you’ll gain access to a live complimentary Free Cash Flow Valuation Tool for over 200 stocks, as well as access to our 3 model portfolios. The paid subscription is only $5 per month and you can cancel any time.

In case you missed them here are some recently covered stocks

HCA Healthcare Inc. HCA 0.00%↑

Texas Roadhouse Inc. TXRH 0.00%↑

Also check out some tools to help with your investing journey

Stock Valuation Tool (version 2)

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin