Valuing the Quality Portfolio

New Valuation Technique

I recently added another valuation method to my arsenal of measuring intrinsic value. The newly minted valuation leverages Free Cash Flow per share and it is applied in a similar fashion as the P/E multiple valuation.

Currently I am running a backtest to measure the effectiveness of all three valuation methods. In the previous valuation test I observed that the application of Dividend Yield Theory and the P/E multiple yielded positive alpha over the universe of stocks tested. Applying both valuation methods together also showed promising results. It’ll be interesting to see how the FCF/share multiple stacks up against the two other valuation methods, and whether a more comprehensive combination of all three methods will yield superior results as well.

Performance Update

Today, I’ll provide a quick update on the performance results of the portfolio for partial February and I’ll share with you the current valuations for all 25 included stocks.

Through February 16th, the price only return for the portfolio stands at +3.74% relative to +3.44% for the S&P 500 and +0.97% for SCHD. This brings the YTD return for the portfolio to +5.10% relative to +5.08% for the S&P 500 (measured by SPY) and +1.11% for SCHD.

The valuation tilted version of the portfolio has a partial return of +3.02%, so thus far it is not yielding alpha over the standard portfolio. The YTD return for the valuation tilted portfolio stands at just +3.20%. As a reminder the valuation tilted portfolio has an outsized allocation to: ADP, JNJ, MKTX, TSCO and ZTS (all 8%) with the remaining 20 stocks all having a 3% allocation.

Four stocks are driving the portfolio return in February:

AMAT +21.47%

MPWR +21.20%

LRCX +12.22%

KLAC +11.33%

Dividend Growth

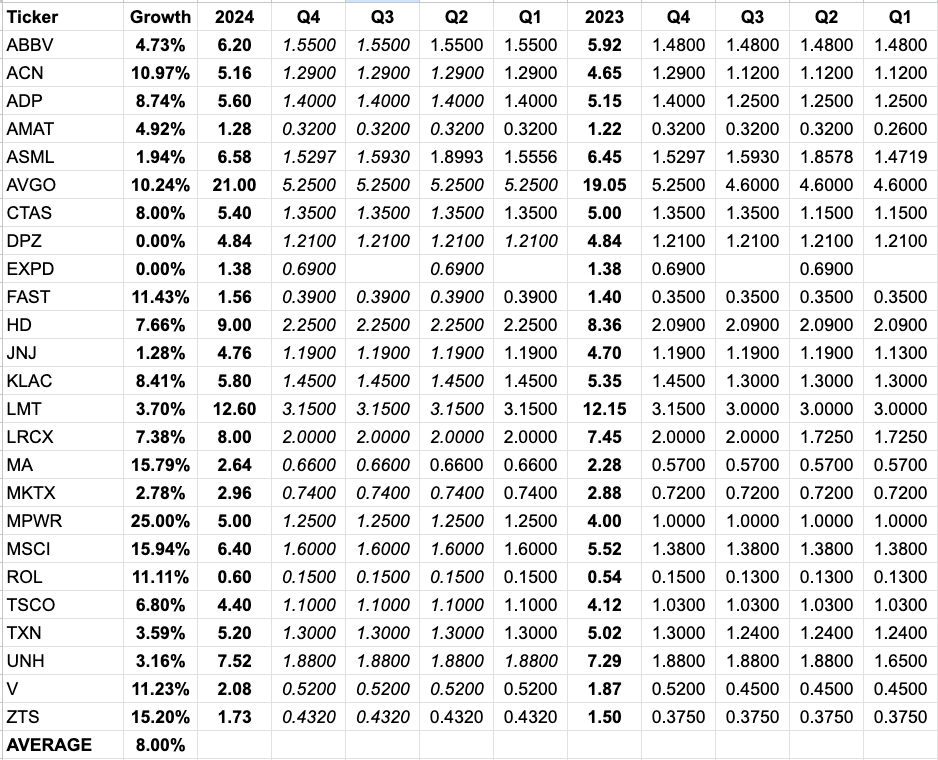

Seeing how this is a high quality dividend growth portfolio I think its useful that I track the dividend growth the portfolio delivers. I know that we are only 1.5 months into the year but several of these stocks have already raised their dividend payouts for 2024. We can also project some organic calendar year dividend growth based on dividend increases from the prior year. As of right now the dividend growth rate for this portfolio stands at a flat 8% (2024 annual dividend vs. 2023 annual dividend). Seeing how many of the stocks have not announced their 2024 dividend increase yet, its fairly plausible to assume we can see dividend growth in excess of 10%. Here’s a breakdown of the dividend growth as of 2/20/24.

The quarterly dividend amounts for 2024 that are italicized are estimates and will be updated throughout the year as these companies declare future dividend payouts.

Current Valuations

Now onto the fun part, let’s see which of these 25 stocks appear to be attractively valued today.

In the attached PDF you’ll find a full valuation for each stock. Please keep in mind that these valuations are estimates and they rely on the assumption that stocks revert back to the mean in the long run.

Looking forward to this new twist!