Automatic Data Processing (ADP)

Cashing In!

Automatic Data Processing

ADP was originally covered on September 26, 2024 and was trading for about $275 per share at that time. Since then the stock is up about 11% and is trading for $305 right now. Let’s review the company’s most recent earnings report and see where ADP may go from here.

Q3 2025 Earnings

In late April of this year, ADP announced their Q3 earnings with an impressive double-beat. Non-GAAP EPS was $3.06 per share beating analyst expectations by $0.09, on revenue of $5.6B which also topped the consensus by $110M, and was a 5.7% increase compared to Q3 2024.

Revenue

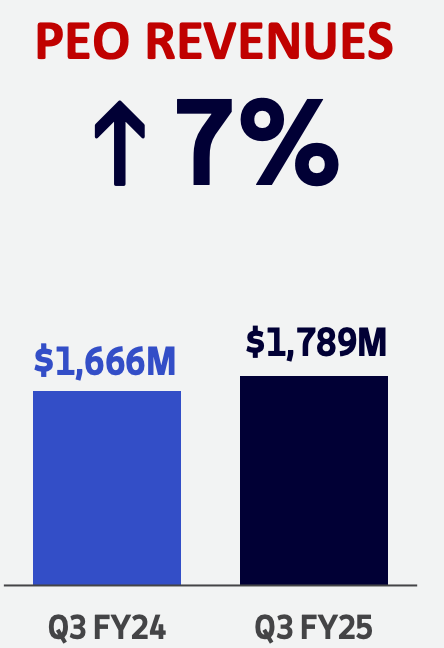

ADP 0.00%↑ has two reportable segments, Employer Services and Professional Employer Organization.

Looking at the Employer Services segment first, revenue rose 5% compared to the same quarter a year ago. The factors contributing to this increase were new business bookings, a better than anticipated retention rate, as well as higher interest on funds held for clients. Additionally, the margin for this segment expanded 20 bps to nearly 40%, driven by growth interest growth on funds held for clients.

The Professional Employer Organization showed a 7% increase in revenue with a strong retention rate the main driver, partially offset by higher wages. The margin for this segment was flat YoY, coming in at 14.2%, with strong revenue growth and a favorable actuarial development was completely offset by higher employee costs.

Fiscal 2025 Guidance

Overall company expectations for 2025 include:

Revenue growth of 6-7%.

Adjusted EBIT margin expected to expand almost 50 bps.

Diluted EPS growth of around 10%.

Adjusted Diluted EPS growth closer to 8.5%.

Employer Services segment:

Revenue growth between 6 and 7 percent.

Margin expansions close to 50 bps.

New business bookings growth around 5%.

Professional Employer Organization segment:

Revenue growth between 6 and 7 percent.

Margin contraction of close to 70 bps.

Also check out some tools to help with your investing journey

Follow on other social media platforms

Link to Youtube

Link to X @LongacresFin

Valuation

The final consideration is to determine if ADP 0.00%↑ is trading for an