To be or not to be, a shareholder of ADP

Intro

While there are many ways to create success in the stock market, I believe there is only one simple way to passively build wealth in the long run. That way is to adhere to the following three rules.

Invest in High Quality Businesses.

Purchase them for a fair or better price.

Hold these positions for as long as rule 1 continues to be true.

Today I am going to take a look at Automatic Data Processing, and tell you why I believe it is a great business, trading for a reasonable price today.

Background

From its humble origins in 1949, the Taub brothers, Henry and Joe, have grown this small payroll processing company to become a global leader of cloud based human capital management solutions. Automatic Data Processing (ADP), originally founded as Automatic Payrolls, Inc., went public in 1961 with 300 clients, 125 employees and annual revenue of roughly $400K. By 1985 the company was processing payroll checks for nearly 20% of the US workforce. Today it is a leader in the human resource management industry with footprints spanning across the globe. Throughout its 70 year plus history the company grew through countless acquisitions but also spun off some of its components. Most notably, in 2007 ADP spun off its brokerage service group to form Broadridge Financial Solutions (BR), another notable quality business on my shortlist.

ADP is the 93rd largest company in the S&P 500 with a market cap just shy of $100 billion. It generates annual revenue of $18 billion and has an outstanding track record. Management is forecasting continued growth in the upcoming year with 6 to 7% expansion in revenue, a 4 to 7% increase in new business bookings and 10 to 12% growth in adjusted diluted earnings per share.

Track Record

ADP went public in 1961 but its difficult to obtain reliable market data going back that far, therefore I have limited my review to 1985. Since 1985 ADP has grown by roughly 20,470%, compared to a 5,585% cumulative return from an equivalent investment in the S&P 500. While its compounded annual growth rate of 14.77% does not look significantly higher than the 11.02% for the S&P, the compounding effect over multiple decades would lead to a final valuation that is approximately four times better. Turning a $10,000 investment into more than $2 million if held in ADP stock versus $550K with the S&P 500.

Not every part of the past 38 years was a fruitful time to own shares of ADP. Comparing the stock to the S&P on a single calendar month basis, ADP outperformed the index 51.51% of the time, giving you a very slight edge on the market. Patient investors that held their shares for a longer period of time generally faired better. On a rolling 12-month basis ADP outperformed the index 60.71% of time. On a rolling 36-month basis ADP outperformed the index 68.07% of time. And on a rolling 60-month basis ADP outperformed the index 84.44% of time.

These results are not quite as impressive as those we reviewed last week with Visa, but ADP has a far longer history on the market and has weathered many more turbulent events. In my opinion, a 84% winning record against the S&P over any 5-year period is quite excellent.

Quality Quadrant

Having an excellent track record is great but let’s see how attractive ADP looks from a business quality perspective. I believe a great place to start evaluating the quality of a business is what I like to call the quality quadrant, 4 financial metrics that help me gauge the operational strength of a business. These metrics are: the return on capital employed, total revenue, gross margin and the free cash flow conversion ratio.

The return on capital employed tells me how profitable a company is and how well it utilizes its capital. Turning capital into profits is the primary driver of creating value for shareholders.

During the past decade ADP has seen its ROCE improve from a low of about 21% in 2013 to slightly above 40% today. While the improvement wasn’t steady and consistent from year to year, taking a step back and looking at the past decade as a whole we can see that the returns have generally improved over time. The rate of improvement has been slowing as can be seen by the 3 year trend of 5.14% being lower than the 10 year trend of 7.04%. ADP earns a perfect 100% quality score for its ROCE.

Revenue is the money a business generates from operations. It is the top line figure of the income statement, and by comparing historical values we can gauge how quickly a business is growing.

During the past decade ADP has seen its revenue grow quite nicely with a minor setback in 2015. Between 2014 to 2015, revenue declined by a little more than 10% and it took nearly two additional years for ADP to set a new all-time high annual revenue figure. During the past decade revenue has grown by about 70% or by nearly 5% per year on average. Because of the minor setback in 2015, ADP receives a quality score of 90% for its revenue history.

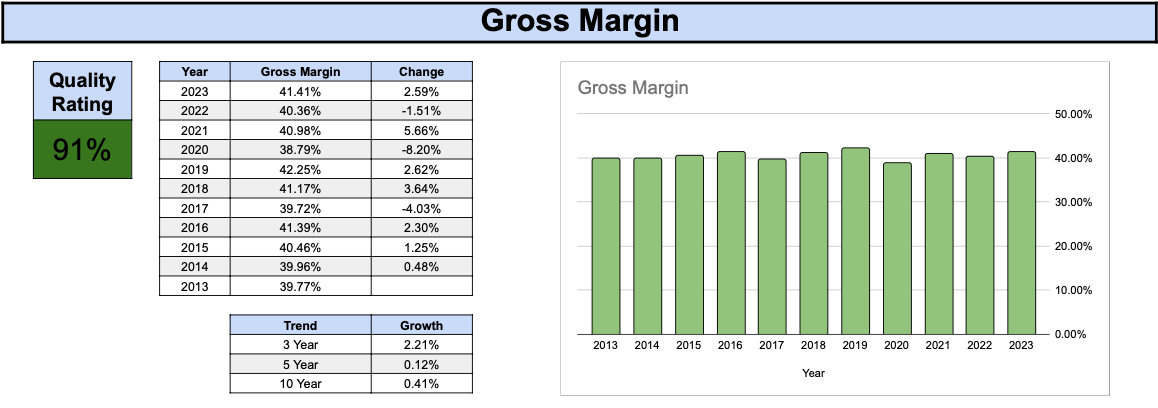

Gross margin is the portion of revenue that is left over after direct costs are subtracted. It is one of the most important indicators of the company’s financial performance. It tells you how much cash the company has to fund operations, service its debt, distribute to shareholders and fund future growth.

During the past decade ADP’s gross margin has remained very consistent right around 40%. Ideally I would prefer a business with a gross margin closer to 50% and for that reason ADP receives a quality score of 91% for this metric.

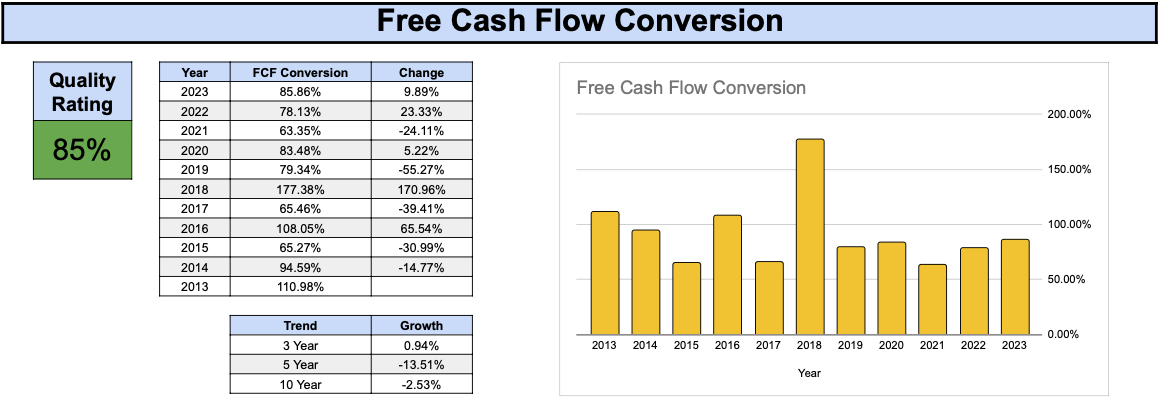

The free cash flow conversion ratio measures a company’s efficiency of turning profits into free cash flow. The point is simple, free cash flow is king, and companies that generate healthy levels of free cash flow have more financial flexibility.

During the past decade ADP has done an swell job at converting profits into free cash flow. The FCF conversion ratio has oscillated between a low of 63% in 2021 and a high of 177% in 2018. While this volatility is not ideal the company has been a cash flow machine. The one negative point we can deduce from the chart is that the FCF conversion ratio has been trending lower, this is further supported by the 10 year trend sitting at -2.53%. For this reason ADP earns a quality rating of 85% for this metric.

Combining the quality ratings for all 4 metrics ADP earns a composite quality score of 91.5%. In my opinion any company with a score above 90% is of the highest tier in terms of business quality. While there are many other aspects that need to be evaluated when performing sound due diligence, screening for the quality quadrant is a great place to start. I leave the rest up to you.

Dividend History

ADP has a 48 year history of paying and increasing dividends, earning them a spot on the coveted dividend aristocrat list. Pretty soon they will be further elevated to the status of a dividend king as I foresee their strong dividend history continuing for many years to come.

For a company that has paid a continuously growing dividend for nearly 5 decades, ADP has a very strong dividend growth history. During the past decade the dividend has increased by nearly 13% per year on average, with only three out to the last ten years seeing less than double digit dividend increases. Going forward investors shouldn’t expect exceptionally high dividend increases from ADP every year, but based on the growth prospect for the business I believe the long term dividend growth rate should remain very healthy.

An outstanding dividend growth history is only more impressive if it is accompanied by a low and steady payout ratio. During the past decade ADP has managed to maintain its payout ratio at a pretty respectable range right around 60%. The payout ratio has been pretty consistent and actually trended slightly lower more recently.

Valuation

Valuation is more art than science but at the end of the day you do have to come up with some baseline for fair value. I like to leverage two techniques to help me gauge how attractive a given stock is. Those techniques are dividend yield theory and the price to earnings multiple valuation.

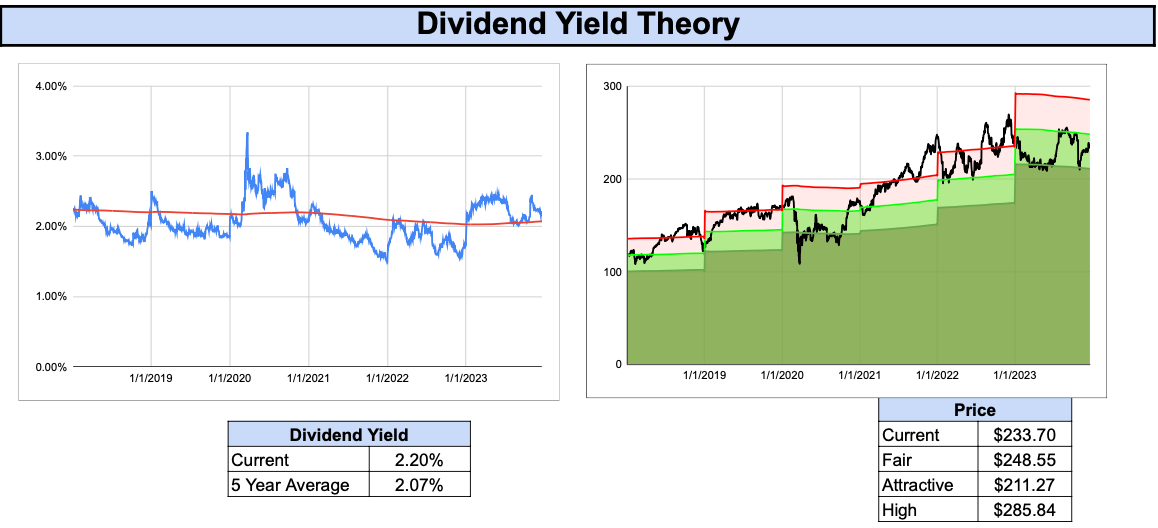

Let’s take a quick look at dividend yield theory first.

This valuation technique is quite simple to understand, if the current dividend yield is higher than the trailing average dividend yield the stock is presumed to be undervalued, and vice versa. In the left chart below you can see ADP’s historical dividend yield (blue line) compared to its 5-year rolling average dividend yield (red line). As you can see the dividend yield has moved within a range of about 1.5% to 3.25%, but generally it’s oscillated around 2%. The 5 year trailing average dividend yield currently sits at 2.07%, indicating that when the actual yield exceeds 2% ADP is reasonably valued. Based on this valuation model, dividend yield theory suggests that a fair price for ADP today is somewhere in the range of $248.

Let’s see what the price to earnings multiple can tell us.

During the last 7 years ADP has traded for a 20 to 40 multiple of earnings. Today it sits somewhere in the middle with a P/E ratio of 27.66. The trailing 5 year average P/E ratio is 29.93 indicating the stock is potentially slightly undervalued. While a P/E ratio of nearly 30 is considered expensive in the context of the broad equity market, ADP as a quality business generally demands a premium price. The recent P/E ratio history suggests a fair price of about $253 for ADP today.

While both valuation methods indicate ADP is potentially undervalued today I don’t like to put too much emphasis on their accuracy. Therefore I would conclude that ADP is reasonably valued today and may potentially be slightly undervalued as indicated by dividend yield theory and the trailing P/E multiple.

Final Thoughts

I have a long position in ADP with the intention of owning the business so long as I believe it to be quality company. I encourage you to do your own due diligence beyond the scope of the brief analysis I presented, to determine for yourself if you also believe that ADP is a great business and whether or not the valuation today makes sense to you.

Great analysis! ADP’s been on my shortlist and now I am even more comfortable with my purchase from this morning. Thanks!