Is Chasing Excess Returns Worth The Trouble?

Let’s not kid ourselves, everybody wants to see above average returns in their portfolio. The problem is that this won’t always be the case. And to make matters worse chasing higher returns often times leads to below average results. You have to ask yourself if the juice is worth the squeeze? But before you answer, you should consider which juice is more advantageous for you to squeeze. If that didn’t make any sense at all I promise you it will by the time you finish reading.

Basic Passive Investing

The best type of long term investing is the simplest form of investing, that is of course a passive style of investing. With this form of investing you’re not making a whole lot of decisions, all you do is invest periodically into a basic portfolio and you let time work to your advantage. If we consider the 3 largest dividend ETF’s in terms of assets under management (AUM): Vanguard’s High Dividend ETF (VYM), Vanguard’s Dividend Appreciation ETF (VIG) and Schwab’s U.S. Dividend Equity ETF (SCHD). Each of these funds has achieved very respectable long term results and they all come with industry low expense ratios of just 6 basis points (0.06%).

VYM has returned 8.58% per year on average since 2006 and it has a trailing twelve month SEC yield of 2.71%.

VIG has returned 9.76% since 2006 and it’s trailing twelve month SEC yield is 1.70%

If we normalize SCHD’s long term return back to 2006 using VIG as a proxy it would be roughly 9.60% and it’s trailing twelve month SEC yield is 3.63%.

Assuming each of these funds will compound at the same rate over the next 20 years as it has over the past 18, here are the type of results we can expect from religiously investing $500 per month.

VYM

$317,992.21 Market Value

$62,536 in dividends paid (reinvested)

$7,936.63 in dividends paid in year 20

132% dividend return relative to annual contribution in year 20

VIG

$367,062.33 Market Value

$43,033.40 in dividends paid (reinvested)

$5,685.19 in dividends paid in year 20

95% dividend return relative to annual contribution in year 20

SCHD

$359,774.16 Market Value

$90,702.71 in dividends paid (reinvested)

$11,916.32 in dividends paid in year 20

199% dividend return relative to annual contribution in year 20

In my opinion these are phenomenal results for the minimal effort required to setup this investment. All you would need to do is have the $500 in disposable income each month, deposit it into your brokerage and invest into the dividend fund of your choice. Today, many brokerages will allow you to setup this exact investment strategy and have it run on autopilot. This means it shouldn’t take you any longer than 30 minutes to an hour to set this up. After that you can enjoy the next 20 years doing whatever makes you happy and let this investment strategy run in the background.

For perspective, investing $500 per month for 20 years equates to a total investment of $120K. This means that if these funds could potentially triple the value of your money and on top of this compounding you’d be building a solid stream of passive income.

But perhaps you’d like to achieve better results over the next 20 years?

Chasing Better Returns

Earning a higher return from the market not only requires you to take on more risk, it also requires more effort on your part. Risk is a funny concept in the investing world. Most professionals define and measure risk as volatility. Most people perceive “risk” as the potential of experiencing a loss, but “risk” or volatility in the market simply measure how much and how quickly an asset has historically moved relative to the broad market. In theory when you invest in an asset that has historically been more volatile than the market you may continue to see the value of this asset swing more than the market, in both directions. Of course there are other elements that come into play such as the initial purchase price of the asset, the fundamental growth of the asset and investor sentiment that will drive returns. All of these factors may cause an individual asset to deviate from historical patterns.

Suffice it to say, if you want to see higher highs you have to accept that you may also see lower lows. The lower lows may never materialize but the probability of them occurring increases when you invest in assets that have historically been more volatile.

The second element of chasing higher returns is that it requires more effort on your part. Finding assets that have the potential to offer above average returns is not easy, many investors try and fail to do this everyday. It takes time to learn how to find these assets and then of course additional time to actually go out and identify opportune times to invest in these assets.

One good way to look at it is by considering the value cost proposition. The value cost proposition defines the value of something as the benefit less the cost. Let’s define the benefit as excess return and the cost as your time.

Measuring The Value of Earning an Excess Return

Let’s use VYM as an example. To refresh your memory, VYM has grown at an annualized rate of 8.58% since 2006. If we assume that you’re planning to invest $500 per month into VYM for the next 20 years. And if we assume it can duplicate its long term CAGR of 8.58% during this period of time. You’d end up with $317,992.21 if you reinvested all dividends along the way.

But what if you’d like to have a higher market value 20 years from now? The simplest way to do this is by either investing more money into VYM each month or by complementing this asset with a faster growing asset in your portfolio. So how do you decide which route is better for you? The keyword here is YOU.

Let’s break this problem down by considering the cost of your time. You can either commit your time to find an alternative asset that will generate a higher return than VYM or you can commit your time to earn/save and invest the additional capital required to increase the ending market value of your VYM investment to meet your desired goal.

In a fixed growth forecast model we can compute the tradeoff between these two options. Generating a 1% higher rate of return (8.58% * 1% * 100 = 8.67%) would lead to an additional $3,400 in ending market value. The same result can be achieved by investing 1.2% more money each month, that’s roughly $6 extra dollars per month. It’s worthy to note that attempting to increase your return by adding an alternative asset to your portfolio carries the risk (volatility) of potentially ending up with a worse return relative to investing solely in VYM. While investing additional capital does not carry this same risk.

Earning or saving an extra $6 per month seems like a fairly easy task. On the other hand earning an additional 9 basis points per year is also fairly simple with a more growth oriented asset, and the potential risk can be weathered over a 20 year period of time. Whether you will like the added volatility in your portfolio is a completely separate consideration.

What’s interesting to note though is that this relationship between earning a higher rate of return and investing additional capital is linear. Every 1% increase in the rate or return is equivalent to a 1.1-1.2% increase in invested capital. Both options end up generating the same final result (market value), in this fixed example of investing in VYM.

Going back to which juice is better to squeeze. You should consider which of these two avenues to a higher ending market value will leave you happier. Time is your most valuable asset and how you spend your time should matter. So which task will be easier and more enjoyable for you? Researching alternative investment options or earning/saving extra income that can be invested?

I personally enjoy reading and studying about various stocks and investing strategies, this activity brings me pleasure. But I also found a way to partially monetize this activity as I earn a little bit of extra income through sharing my ideas and thoughts online. Sort of killing two birds with one stone. However, if my hobby of choice did not involve the stock market, a better way to spend my spare time over the next 20 years may be thinking of ways to monetize my hobby to create more capital to invest rather than researching the stock market.

If I were to fully invest into VYM for the next 20 years, my outcome will not be any better or worse than VYM over this time period. But if I were to add an alternative asset into a portfolio with VYM my outcome may be better but it may also end up being worse than investing solely in VYM.

If you have a hobby that you can monetize and earn $100 extra per month that you could invest into VYM, it would be the equivalent of earning a roughly 17% higher return (8.58% * 17% * 100 = 10.04%). And both options would compound to an additional $62K in market value over a 20 year period if VYM can grow at its historical average rate of return.

What Make You Happy

It’s worthy to think about the concept of where you should devout your spare time. Life will pass by very quickly whether you like it or not. If researching stocks is not your cup of tea, and if investing in individual stocks bring you additional stress it may not be the right option for you.

If you figure out what makes you happy, find a way to monetize it and invest that excess income, and you can duplicate the effect of chasing higher returns without the necessary effort or undue impact of feeling excess volatility. You may also find that when you look back and reflect on the next 20 years your memories will be more pleasurable.

Ideally you want to pursue both these options, find calculated ways to improve your overall return and find additional capital you can put to work in the stock market. The best place to start is with whichever of these two routes is simpler for you today.

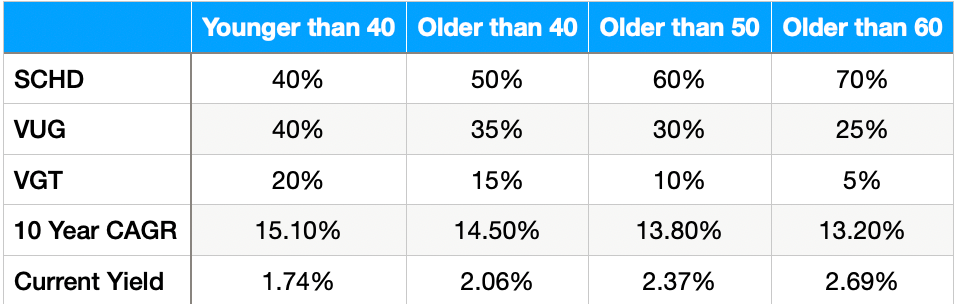

Designing A Simple Portfolio

Here’s a basic asset allocation I have recommended in the past for anyone looking to create an easy ETF portfolio with a focus on growth and income. I’ll break it down by age group.

Each of these portfolios has compounded at a much faster rate relative to VYM (9.8%) and VIG (11.7%). What these portfolios don’t offer is a high starting dividend yield. However, with enough time and enough invested capital they will still generate a healthy amount of growing dividend income.

Have a great rest of your Thursday!

Thank you good Sir, excellent article. Always enjoy them and your podcasts!

Great article. Really enjoyed the perspective of valuing one’s time as an asset, the scarcest of all assets. Enjoy your Patreon writing as well - thank you for your thought and action provoking writing and research.