How Did Monolithic Power Systems Manage To Beat The S&P 500 Index 87.72% Of The Time

The Company

Monolithic Power Systems, Inc. (MPWR) is a semiconductor company that designs, develops and sells integrated power solutions. Their focus is on six end markets: data storage, enterprise data, automotive, industrial, communications and consumer. The business was incorporated in 1997 and begun trading publicly at the end of 2004. During its nearly 20 year span on the market the stock has rewarded long-term shareholders with above average returns. On average, an investment in MPWR has grown at rate 3X faster than the market average (measured by the S&P 500 total return).

Streak of Beating the S&P 500

During its history of 230 full calendar months, Monolithic Power Systems has averaged a 2.55% monthly return, relative to a 0.87% return from the S&P 500 over the same span of time. Measuring the stock on a rolling 5-year return, at each month end, we have 171 data points that can be compared to the S&P 500. Monolithic Power Systems has outperformed the index during 150 of these rolling periods (87.72% rate of success). This outperformance is better visualized in the chart below.

And this chart that shows the margin of over/underperformance.

As you can see, between late 2010 and 2014 the few periods where Monolithic Power Systems struggled to outpace the index, the margin of underperformance was relatively low. However, since late 2014, the margin of outperformance substantially improved, peaking at over 600%, and not falling lower than 150%. The current streak of outperformance stands at 111 rolling 5-year periods, that’s 9 and 1/4 years.

This impressive long-term return did come with considerably more volatility compared to the index.

Out of the 230 monthly returns 139 were positive, on average seeing Monolithic Power Systems rise by 9.59%. Out of the 139 positive months, 51 were in excess of 10%, with the largest monthly gain being 51.12% (October of 2005). Conversely, during the 91 months of negative returns the stock, on average, fell by 8.19%. Out of these 91 negative months, 28 were in excess of 10%, with the worst monthly loss being 43.67% (November of 2008). This means that approximately 34% of the time, shareholders of Monolithic Power Systems saw a gain or loss of more than 10% during any single calendar month.

For context, the S&P 500 index had 155 months of positive returns during the same span of time, on average rising by 3.21%. Out of these 155 positive months, only 3 were in excess of 10%, with the largest monthly gain being 12.81% (April of 2020). The S&P 500 also had 75 months of negative returns, on average losing 3.96% per month. Only 3 out of these 75 negative months saw the index fall by more than 10%, with the largest loss being 16.79% (October of 2008). So while the odds of seeing a gain or loss of more than 10% with Monolithic Power Systems stood at roughly 34%, seeing a similarly high gain or loss with the S&P 500 index happened roughly only 2.6% of the time.

Volatility is opportunity for patient investors with a long-term mindset, but it’s not for everyone. The past 19 years tell us that dollar-cost-averaging into Monolithic Power Systems would have led to excellent, market beating returns, regardless whether the stock was over or undervalued. I’ll circle back to valuation in a second but first lets address the question at hand, how was MPWR able to generate such high rates of return, far exceeding market averages.

High Quality Business

The main reason why Monolithic Power Systems was able to grow at 3X the rate of the S&P 500 was because it is a high quality business, it has a competent management team and it has made smart decisions along the way.

Monolithic Power Systems distinguishes itself from its competitors in several ways.

It’s known for its highly integrated solutions, combining multiple functions into a single chip. This integration reduces the need for external components, simplifies system design, and often leads to smaller, more compact product designs compared to competitors.

The company places a strong emphasis on efficiency across its product portfolio. By developing advanced circuit topologies and leveraging innovative semiconductor processes, its products often exhibit superior energy efficiency compared to those of its competitors. Examples would be longer battery life, reduced power consumption, and lower operating costs for end-users.

They specialize in miniaturizing power management solutions. Their products are designed to be compact and space-efficient, making them ideal for applications where size constraints are critical, such as wearable devices, IoT sensors, and portable electronics.

The company works closely with customers to understand their specific needs and provides tailored solutions. This collaborative approach allows Monolithic Power Systems to develop application-specific products and offer specialized technical support, giving them a competitive edge in industries with unique power management needs.

The company is committed to continuous innovation in power management technology. They invest heavily in research and development, staying ahead of emerging trends and technologies in the semiconductor industry. This enables the company to introduce new products with advanced features and performance capabilities, keeping them competitive in the marketplace.

The company places a high emphasis on the reliability and quality of its products. Through rigorous testing and quality assurance processes, they ensure that their components meet or exceed industry standards for performance, durability, and reliability. This commitment to quality has earned them a reputation for producing dependable power management solutions.

Financial Metrics

Let’s evaluate how attractive Monolithic Power Systems looks through the lens of business quality. I believe a great place to start evaluating the quality of a business is what I like to call the quality quadrant. This quadrant comprises four key financial metrics that serve as reliable indicators for gauging the operational strength of a business. These metrics are the return on capital employed, total revenue, gross margin and the free cash flow conversion ratio.

The return on capital employed tells me how profitable a company is and how well it has utilized its capital. Effectively turning capital into profits is the primary driver of generating shareholder value.

Over the last decade, Monolithic Power Systems has seen its Return on Capital Employed (ROCE) grow steadily, culminating in a healthy range above 20% today. Although 2023 witnessed a minor setback, with the ROCE temporarily dipping to from 29% to 22%, this is still a respectable figure. The short-term (3 year) trend underscores an overall growth trend, boasting an modest 4.08% improvement. While the long-term (10 year) trend has an even more impressive rate of growth of 11.22%.

Revenue represents the financial inflow generated by a business through its operations. Positioned at the forefront of the income statement as the top-line figure, revenue provides a key indicator for assessing the pace of a business’s growth when analyzed across historical values.

Over the last decade, Monolithic Power Systems has achieved an extraordinary 543% growth in revenue, translating to an impressive annualized growth rate of approximately 20.48%, a commendable pace by any standard. Between 2019 and 2022 the rate of growth in revenues increased exponentially, however in 2023 the company only managed a modest improvement of 1.5%. Given that the semiconductor industry is forecast to grow quickly in the next decade, and Monolithic Power Systems is well positioned to benefit from this growth, I believe the future of the company is promising.

Gross margin is the portion of revenue that is left over after direct costs are subtracted. It is one of the most important indicators of a company’s financial performance. This metric shows the cash available for various crucial purposes, including sustaining operations, servicing debt, distributing to shareholders, and fueling future growth.

Over the last decade, Monolithic Power Systems has consistently maintained a robust and stable gross margin, residing in the high 50% range. More recently, in 2023, the company has seen a small decline in its margin, disrupting an otherwise positive long-term (10 year) growth trend.

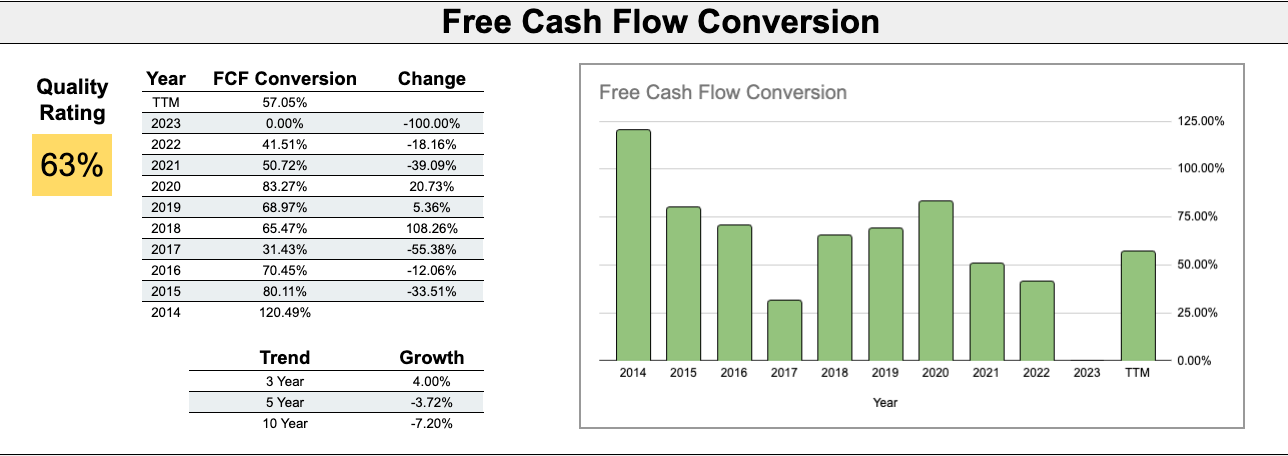

The free cash flow conversion ratio is a measure of a company’s capability in transforming profits into free cash flow. In straightforward terms, free cash flow reigns supreme, and companies adept at generating robust levels of free cash flow enjoy greater financial flexibility.

Over the last decade, Monolithic Power Systems has shown great proficiency in converting profits into free cash flow. While a bit more year-to-year consistency would be ideal, the free cash flow conversion ratio has predominantly held above the 50% mark, with the exception of 2017 and 2022. The chart below lacks data for 2023, but the TTM figure comes directly from the recently announced 2023 financials.

Dividend History

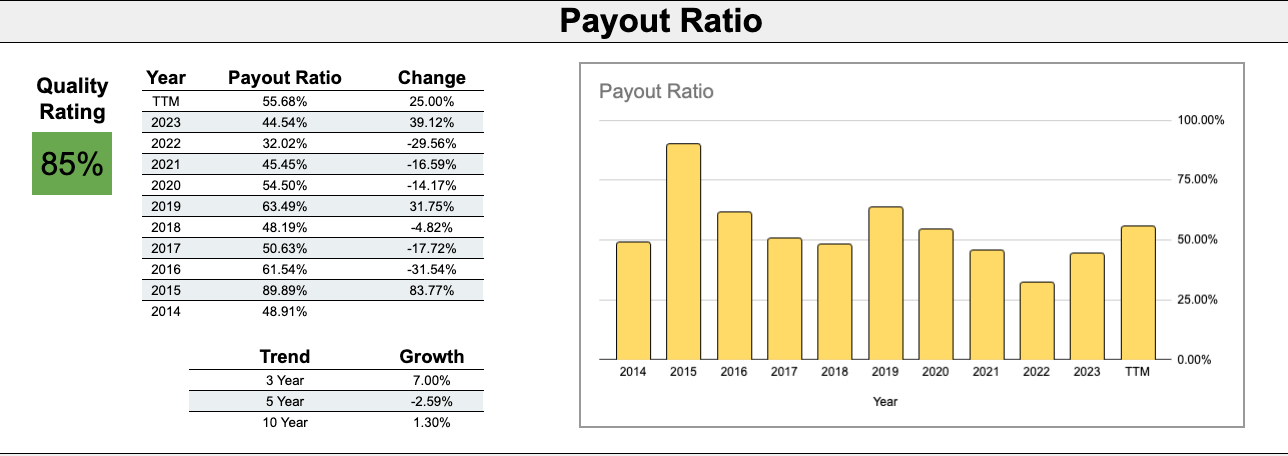

During its 7 year history of increasing dividends, Monolithic Power Systems has consistently maintained an annual dividend growth rate of at least 20%. This pace of growth has not cooled off, with the most recent dividend hikes often times exceeding past years. Recently, Monolithic Power Systems announced a 25% dividend increase for 2024, bringing its annual payout from $4 to $5.

Throughout the last decade, Monolithic Power Systems has maintained a healthy payout ratio, hovering around 50%. For shareholders to continue seeing strong dividend increases, the company will need to grow its operations at an equivalent, fast pace.

Valuation

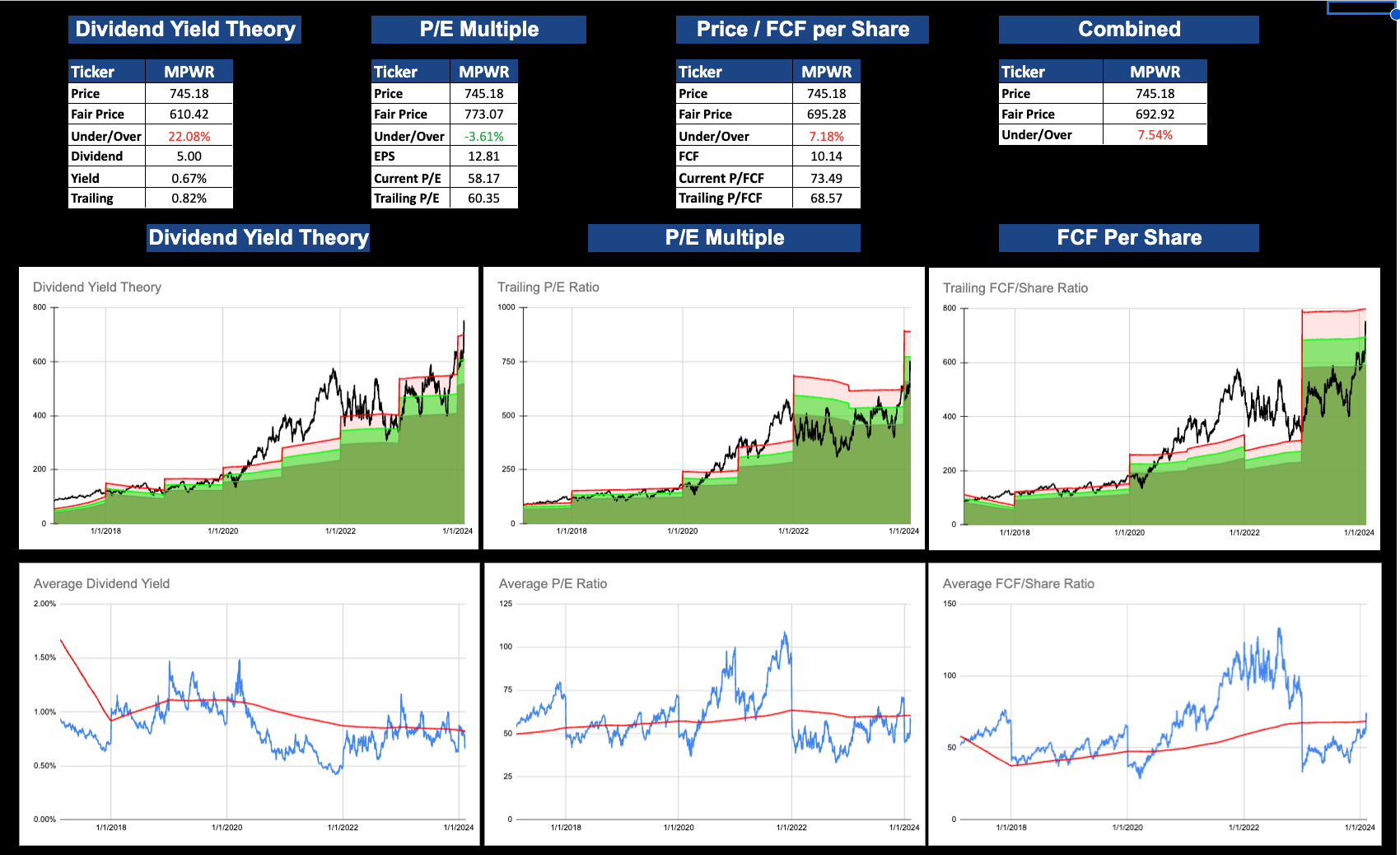

Valuation, though more art than science, requires us to establish a baseline for fair value. To help me with this task, I leverage three techniques to evaluate the attractiveness of a particular stock: dividend yield theory, the price-to-earnings multiple valuation and the price-to-free-cash-flow per share multiple valuation.

In the image below you can see the results of each valuation method, along with historical valuation charts and the average valuation combining all three methods.

The price-to-earnings multiple gives us the most favorable valuation, suggesting Monolithic Power Systems is slightly undervalued. While dividend yield theory gives us the most conservative valuation, suggesting Monolithic Power Systems is significantly overvalued. The price-to-free-cash-flow per share multiple suggests Monolithic Power Systems is overvalued, but trades for a somewhat reasonable price today.

Since late October 2023, the share price of Monolithic Power Systems has nearly doubled, going from a very attractive valuation to a much less enticing entry point today.

Monolithic Power Systems trades for a very high 58X multiple of forward earnings for 2024, estimated to be $12.81 per share. However, analysts are forecasting earnings to grow at a fast pace for at least the next two years. $16.26 in 2025 (26% growth) and $18.92 in 2026 (16% growth).

While history suggests that anytime was a great time to start dollar-cost-averaging into Monolithic Power Systems, I would approach the stock with a level of caution given its very high historical volatility. We may very well see the share price continue its upward trajectory in the months to come and just as likely we could see a sharp pullback, providing a more opportune entry point.

Final Thoughts

I currently hold a long position in Monolithic Power Systems, with intentions of holding on to my shares for as long as I find it to be a high quality company. I strongly recommend conducting your own in-depth due diligence beyond the brief analysis I shared with you today. This way, you can assess whether you share my belief in Monolithic Power Systems as a high quality business and whether the current valuation aligns with your own investment criteria.