3DGR Portfolio Update - May 2024

I felt this image was fitting with how the 3DGR portfolio started out. But the more important question for me is what type of return this portfolio will deliver come April 30, 2025?

For those of you that have followed along, perhaps even made a small bet on this strategy (against my advice), May was a rough month. Things didn’t start out all that bad but as the month went on it kept getting worse.

Day 1. the portfolio underperformed SPY by 2 basis points

Day 2. the portfolio fell behind by another 12 basis points

Day 3. the portfolio clawed back 6 basis points

Day 4. the portfolio gained another basis point

Day 5. the portfolio outpaced SPY by 57 basis points and moved ahead of the benchmark Inception To Date (ITD)

Day 6. we gave the full lead and then some away

Days 7 & 8. we gained the lead back, moving about 25 basis points ahead of SPY

Days 9 through 14. all loses to SPY

Days 15 through 22. the same pattern continued

Ultimately the portfolio finished its first month with a gain of 1.26%. While a positive return is never a bad thing, trailing SPY by 3.8% on the month was quite the gap. And perhaps not the start for this journey I hoped for. But a single months return is irrelevant in the context of a long-term investing strategy.

The S&P 500 is one of the hardest indices to beat, most professional investment managers fail to do so in the long run. It’s actually not ideal to measure the performance of this strategy against this benchmark. We neither used the S&P 500 as the original universe of stocks to create the portfolio, nor do we have the same objective. But the reason why I like using the S&P 500 as my measuring stick is because its a great alternative investment strategy to whatever strategy you follow.

Investing in an index fund that tracks the S&P 500 is one of the cheapest and simplest strategies you can follow. Historically it is also one that has rewarded long-term investors with adequate returns. Therefore I think its a great alternative benchmark to measure yourself against. If whatever strategy you are following isn’t beating the S&P 500, and your overall investing goal is to maximize total return, why not simply park your money in an index fund that tracks this benchmark.

The S&P 500 is heavily weighed towards the “magnificent 7”, and most were not part of our original investable universe. Hence, if any or all of these 7 companies perform exceptionally well, it’ll be tough for the 3DGR portfolio to keep up. I remain optimistic that this strategy will yield better than expected returns in due time.

Here’s what is pretty much guaranteed from the stock market.

1 out of 3 years we will see a correction of more than 10%

1 out of 3 years we will lose to the overall market

The remaining 2 years will more than offset these losses

Things won’t always play out this way, we may lose 2 consecutive years followed by 4 great years. But in general these 3 statements are a good outlook for how to view your returns.

Breaking Down The Portfolio

Let’s start with the overall returns again.

SPY +5.06%

3DGR +1.26%

Investable Universe +2.87%

alpha -3.80%

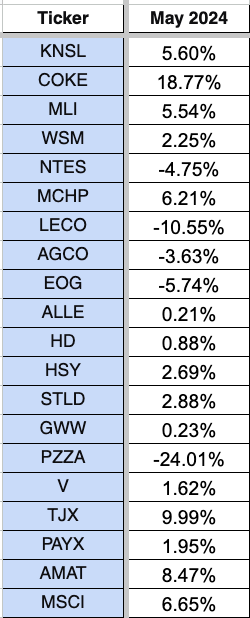

Here’s how each of the 20 chosen stocks performed in May.

The strategy managed to pick a few good stocks.

COKE +18.77%

TJX +9.99%

AMAT +8.47%

But it also lumped in some of the biggest losers from the investable universe.

PZZA -24.01% (worst stock in the universe)

LECO -10.55% (3rd worst stock in the universe)

In total 7 stocks beat SPY in May with the remaining 13 underperforming.

Here’s a heat map for each stock on each day.

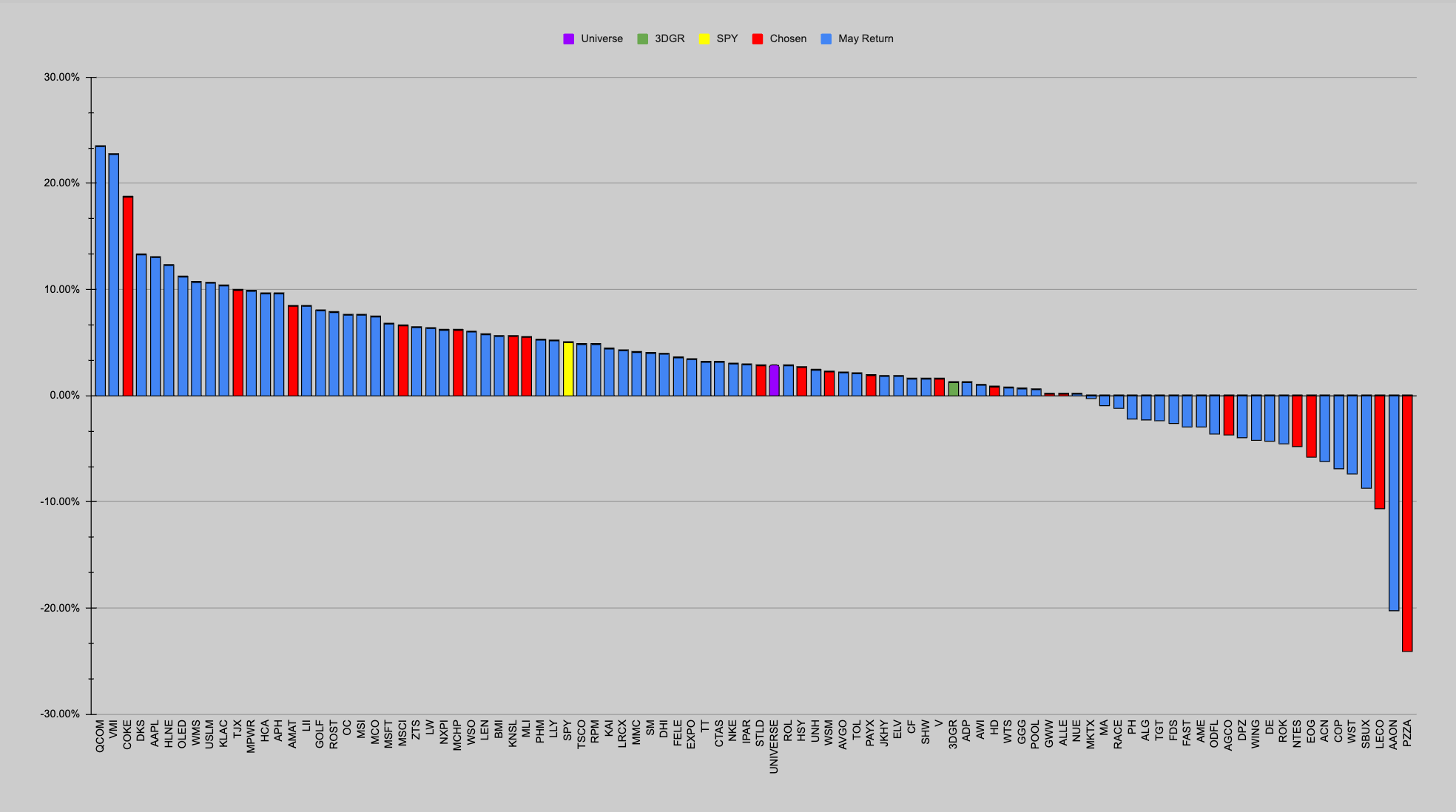

And a chart showing the return for all of the stocks in the universe, SPY, the 3DGR portfolio and the average investable universe return.

Now comes the tough part. 11 months of patiently waiting for this strategy to work, with no guarantee that it will.

Conceptually the strategy still makes sense to me and therefore I will patiently stay long.

As for my actual portfolio, the hurdle is a bit larger than the model return data I just went over.

The return for my portfolio for the month of May was +0.76%. The difference here is that there were a few missed dividends during the month (the model returns are all total returns) and I was not able to set the allocation to each stock at equal weight. I relied on M1’s rebalance feature to do this for me and while it works great it does have its faults. The rebalancing takes place while the stock market is open, so day 1 for my portfolio was worse than the model portfolio return.

As I’m writing this update the first trading day in June is coming to a close and it looks like the portfolio will start this month trailing SPY again. SPY is up 0.08% while the average return for the 20 chosen stocks is -0.79%.

While I haven’t made any key observations about this data yet, I have considered whether the model strategy could have taken a different approach to valuation. As is, the model portfolio measured valuation simply by comparing the FCF Yield for all 93 companies in the investable universe. Perhaps a better approach would have been to measure valuation on an individual basis, comparing each individual company’s FCF Yield to its trailing average. In the coming months I will analyze this data and share with you the results. If the outcome will be favorable it may be one of the optimization adjustments to this strategy for fiscal year 2.

For now I will patiently watch the portfolio to see how it fairs in the days to come.