3DGR Portfolio - June 2024 update

The second month for this portfolio was equally as awful as the first, the 3DGR portfolio fell by 0.33% in June, trailing SPY by 3.86%. Two months, two big losses, what’s going on?

Well, either this strategy doesn’t work as well as the backtest suggested it might or our timing is pretty awful and the portfolio was kicked off during a sour patch for this investment style. There are not excuses in math, the numbers are what they are, and they are not too great.

After 2 months the portfolio is up 0.93% and is trailing SPY by a whopping 7.84%. July also has not started out too well, the portfolio has lost another 0.17% through mid-day 7/9, meanwhile SPY has added 2.06%. This extends the since inception loss to 10.25%, a hole that will surely be difficult to climb out of in the next 9.5 months.

I’ve been scratching my head trying to think of anything I may have missed or overlooked in the initial research and the backtest. Perhaps the fact that the backtest ran neatly using calendar years and I started this portfolio on a random May might be the culprit here. Personally, I don’t believe that should matter too much. I also considered whether I placed too much focus on finding a model strategy that led to the best outperformance, rather than focusing on models that made the most conceptual sense.

We also have to consider that the S&P 500 has been stubbornly exceptional recently, driven by the magnificent 7 and fueled by AI optimism. Dividend oriented strategies are not known to beat the average market return, especially during periods of euphoric growth. Seeing how this portfolio has limited exposure to technology and does not include the magnificent 7, we may be in for a bumpy first year.

This is the dilemma of relying on historical returns, they aren’t always indicative of future results. That being said we are only 2 months a few days into the 3DGR journey and I’m going to give it a runway to prove its worth.

Let me breakdown the portfolio return first and then I’ll touch on a few other points.

3DGR - June Returns

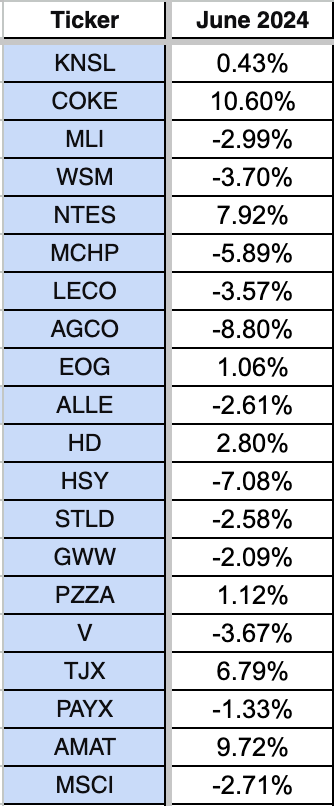

Collectively the 20 stocks in this portfolio fell by 0.33% last month. 8 of the 20 stocks saw positive returns during the month while the other 12 finished the month in the red.

The biggest winner was COKE with a gain of 10.6%. AMAT came in a close second place with a gain of 9.72%. And an honorable mention goes to NTES with a gain of 7.92%.

The worst losers were AGCO with a loss of 8.8%, HSY with a loss of 7.08% and MCHP with a loss of 5.89%.

Here are all of the individual returns for June.

Since inception there are 3 clear winners in this portfolio.

COKE +27.74%

AMAT +25.52%

TJX +19.39%

But we also have 3 pretty big losers.

PZZA -28.76%

AGCO -13.56%

LECO -13.03%

Here is the monthly return data for the portfolio with some color coding to highlight the winners and losers for each day.

And one more chart showing the full investable universe, the return for the 3DGR portfolio, SPY and the investable universe as a whole.

Going Forward

What I would like to see going forward is for this portfolio to perform better relative to SPY. I don’t really care if it loses 3 or 4 months in a row to the index so long as its relatively close, preferably ahead of SPY, after the full 12 months. I’m staying optimistic even though its becoming more and more difficult.

My Actual Portfolio

The M1 Finance portfolio I have dedicated to this strategy is fairing about as well as the model portfolio I summarized above.

It performed a little better than the model portfolio in June, finishing the month flat (it was actually up by $0.25 but that was less than 1 bp).

The portfolio’s return for the period May - June is +0.77%, placing it 0.16% behind the 3DGR portfolio summarized above. If you recall my actual portfolio underperformed in May due to the initial balancing of the stocks as I relied on M1’s rebalance feature to do this on the first trading day.

I’ll have a more detailed update on this portfolio including dividend analysis in the future.

Future

I’ll be running and sharing a few additional backtests on the original dataset to find potential optimizations that can be implemented for the second fiscal year. Those tests will revolve around a more concentrated initial investable universe and a different valuation technique than the FCF Yield. The analysis will be presented in future newsletters.

Thank you for reading, I hope you have a great rest of your day!